Key fundamentals indicate bright outlook for housing market in 2025

Dr Andrew Golding, chief executive of the Pam Golding Property group

Dr Andrew Golding, chief executive of the Pam Golding Property groupBy Dr Andrew Golding, Chief Executive of the Pam Golding Property group

With loadshedding suspended in March, several fuel price cuts, lower inflation and the formation of the GNU (Government of National Unity) key milestones in 2024, coupled with the prospect of further interest rate relief, South Africa’s residential property market has responded positively with increasing activity and interest as a result of a more positive economic and political outlook. We have already seen national house prices gather momentum, rising to +4.9% in September 2024.

The election in May 2024 was a turning point for the economy, resulting in increased business and consumer confidence, which in turn impacted positively on the housing market. Lower inflation, aided in part by five consecutive fuel price cuts, eased pressure on household finances while the first interest rate cut in September reduced the cost of servicing debt. Globally, inflationary pressures are subsiding with all major central banks cutting interest rates – including the Federal Reserve Bank.

Consequently, there is growing optimism regarding the economic growth outlook with marginal upward revisions and the possibility of even stronger growth.

As far as the housing market is concerned, there are three important influences taken into account:

- Demand – a young population such as South Africa’s provides a steady source of demand for accommodation

- Confidence – now at a five-year high – ensures that people are willing to buy a home

- Household finances – buyers need to be able to afford a home and as interest rates decline and household finances improve, affordability returns.

Encouragingly, the second two factors have improved noticeably during the second half of the year and look set to continue to improve throughout 2025.

While interest rate relief tends to impact the market with a bit of a lag and September’s reduction was only 25bps, household finances will continue to improve, which will also make homes more affordable, so there is upside potential for sales activity in 2025. Furthermore, banks continue to support the housing market with elevated approval rates, declining deposits – currently at a record low, and competitively priced home loans.

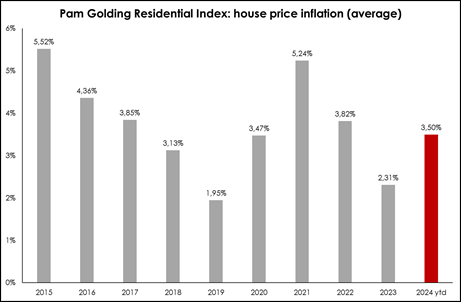

House price inflation over the past year

Source: Pam Golding Residential House Price Index

During the year to September 2024, national house price inflation (HPI) has averaged 3.5% – marginally exceeding 2020’s 3.47% and almost matching 2022’s 3.82%. Depending on Lightstone’s later revisions, it may well be the strongest growth in prices (other than 2021) since 2016.

Notably, as a result of recovery in HPI gathering momentum and inflation easing, real HPI has been positive for two consecutive months. Inflation is set to remain subdued for the next couple of years and if the recovery in house prices continues to gather momentum, we are set for a sustained period of real growth in prices – albeit single digits – which we haven’t seen since 2007.

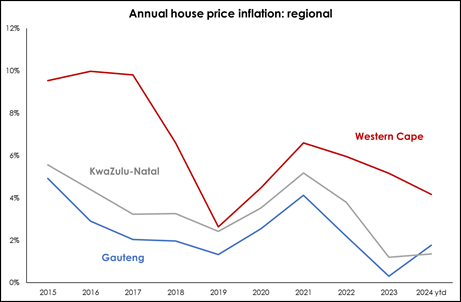

Regionally, over the past decade Western Cape house price inflation has outperformed relative to the other major regions and is currently stabilising at higher levels, while HPI in both Gauteng and KwaZulu-Natal is rebounding and in fact, all major metro markets are showing signs of recovery.

Source: Pam Golding Residential House Price Index

Luxury Market

The luxury sector of the market has shown remarkable strength and is benefiting from increasingly positive sentiment, resulting in a shortage of stock in prime locations which is placing pressure on pricing. Recent high-end residential properties sold by Pam Golding Properties include transactions north of R20 million to close to R100 million and beyond. These include homes sold for R66 million and R60 million in Clifton and Camps Bay respectively, sales for R45.5 million and R54 million in Constantia and other high-end sales in Bishopscourt, a residential sale in Val de Vie in the Cape Winelands for R34.5 million registered in 2024 – which at the time of the sale in 2023 was the highest price achieved in the estate, and a home in Pearl Valley also in the Winelands which sold for R23 million, a vacant stand of over 4 000sqm sold for R25 million and homes which achieved R26 million and R23 million in Steyn City in Fourways, Johannesburg, and a home in Cornwall Hill in Pretoria which sold for R24.9 million, while in KwaZulu-Natal we recently sold two frontline beachfront homes with panoramic sea views in uMhlanga for R17 million and R15 million respectively.

From a group perspective our total sales for the month of October 2024 alone were R2.35 billion, which is 15% ahead of October last year, and which augurs well as we enter the busier summer season.

Key Trends

Semigration

Lightstone data shows a surge in semigration among homebuyers in the wake of the pandemic – with the percentage of those semigrants relocating to the Western Cape rising from 40% in 2019 to 68% in 2023 (no figure available for 2024). There has been a drop-off in semigration in 2024 – perhaps as the relatively high interest rates, and the expense of homes in much of the Western Cape, stems the influx of new homeowners to the province, at least temporarily. According to Lightstone, 25% of homeowners who sell and then buy a new home relocate to another province (Oct’24), while in 2019 it was only 16%. An estimated 50 000 homeowners participated in this sell-to-buy market in recent years. Gauteng and the Western Cape are the dominant regions for these transactions – together accounting for over 70% of this market segment. This reflects a growing desire among homeowners to relocate to another province – particularly in the Western Cape, including the Boland & Overberg and the Garden Route, as well as to Johannesburg, the economic hub of South Africa. Meanwhile, a number of semigrants are opting for smaller towns.

Ongoing demand from first-time and young buyers

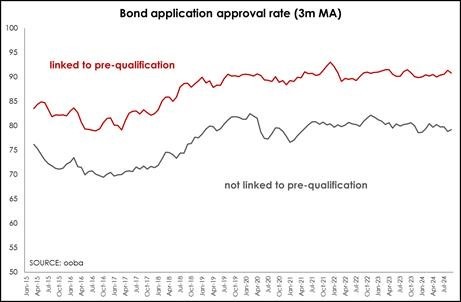

First-time buyer (FTB) volumes slumped by 20% in 2023 according to Lightstone as tough economic conditions took a toll and sidelined potential buyers as a result of pressure on affordability. However, there are signs already that demand from FTBs is recovering as price pressures subside and an interest rate-cutting cycle begins. According to ooba Home Loans, applications from FTBs peaked at 56.2% of applications in May’20 but slowed amidst a resurgence in inflation and a series of rate hikes reaching a low of 44.3% of applications in June’24. Demand has since recovered somewhat – rising to 49.6% of applications in Sept’24 – the highest reading since Nov’22.

There continues to be a clear benefit to obtaining pre-qualification – particularly for FTBs. FTBs who are not pre-qualified experience a lower approval rate than a repeat buyer without pre-qualification but a pre-qualified FTB has essentially the same approval rate as a pre-qualified repeat buyer.

Source: ooba Home Loans

Age of buyers

In 2010, the average FTB was just 33 years old. However, years of sluggish economic growth and the post-pandemic interest rate hikes saw the average age of FTBs rise to almost 36 years as a deterioration in affordability sidelined many potential buyers. However, the average age of FTB is beginning to decline once more – back to 35 years – as economic conditions become more favourable, although differences remain across the regions, ranging from nearly 37 years in Limpopo to just over 34 years in the Western Cape. (Source: ooba Home Loans)

More women buyers

According to Lightstone statistics (July 2024), a decade ago, the largest percentage of homebuyers were mixed-gender couples. However, by 2016 women-only buyers overtook male-only buyers to become second only to couple buyers. In recent years the number of female-only buyers rose steadily while the number of male-only buyers remained steady and in 2022 female buyers became the largest market segment – exceeding both couples and male-only buyers. In terms of existing housing stock, women-only homeowners account for 38% of stock owned and co-own a further 33% as part of a couple, while men-only homeowners account for 29% of all properties. Although women may be buying more property, they tend to dominate in the lower price band – notably the <R750 000 category. Female-only buyers account for the smallest percentage of buyers in the >R1.5 million price band. The gap between prices paid by women-only buyers and mixed-gender couples has widened since 2020, according to Lightstone, presumably due to greater vulnerability to financial pressure.

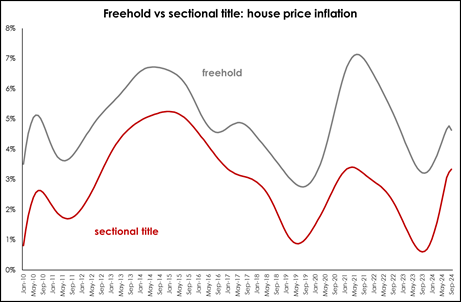

Sectional Title vs Freehold

In 2000 only 13.6% of all residential plans passed were for sectional title properties. In comparison, during the first eight months of 2024, 46% of all residential plans passed were sectional title homes. In regard to sales, the sectional title sector accounted for 23% of total residential sales in 2009 but has now risen to 29%.

Once seen as a first step on the property ladder and a more affordable option, sectional title homes are now embraced as a lifestyle choice, and because downsizing doesn’t mean downscaling, many of those downsizing due to life stage are opting for high-end apartments to enable a lock-up-and-go lifestyle. Developers are responding with a growing percentage of new building plans passed being sectional title, particularly as increased densification occurs in key commercial hubs or metros, such as Cape Town. Also, as demand is concentrated in urban nodes (with SA’s young, rapidly urbanising population) land scarcity makes it necessary to opt for smaller homes. As a result of lifestyle changes and affordability, there is a general shift to sectional title from freehold, not only among home buyers but among developers catering to the increased demand – as sectional title is becoming more appealing when located within a mixed-use development as these offer better location and a broad range of amenities.

Freehold homes outperformed relative to sectional title homes in the wake of the pandemic as people shifted out of cities to smaller towns – where better affordability allowed them to purchase freehold homes. However, according to Lightstone, sectional title house prices are currently rebounding more strongly than freehold prices.

SOURCE: Lightstone

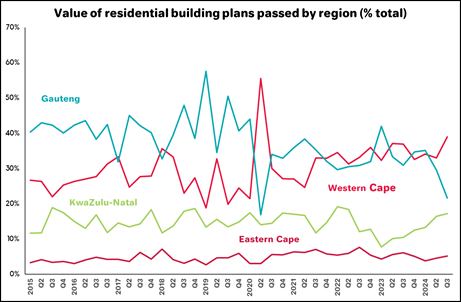

Building plans passed

Source: StatsSA

Prior to the pandemic, the value of plans passed was higher in Gauteng than in the Western Cape. However, in more recent years the two have accounted for a very similar percentage of the total value of plans passed, although in Q3’24 the Western Cape surged to 39% of all plans passed by value while the value of plans passed in Gauteng slumped to just 22%. The other noticeable trend has been the steady rise in the percentage of plans passed in KZN from a low of 7.7% in Q1’23 to 17.2 in Q3’24 – essentially reversing the slump in plans passed during the course of 2022 (probably due to the floods and unrest at the time).

Estate Living

Quality of life and security are the key drivers behind the consistent demand for estate living There is continued robust development in estates, particularly in sectional title homes and retirement developments, as living in estates extends to a wider audience. Some developers have identified this market as a growth sector – but at a more affordable price point than the earlier estates. W hat started as golfing estates has proliferated from being an option only for the affluent to being more broad-based with estates increasingly catering for a wide range of incomes, sometimes within a single estate. The appeal of estates is obvious – primarily security and the delivery of services but also the lifestyle offering – with access to shared facilities that many homeowners would not be able to afford on their own, as cost and maintenance are shared across all homeowners – regardless of income. This can range from small golf estates to essentially ’private cities’ with schools and business centres within a larger estate.

According to Lightstone, in 2009 just 11% of all homes sold were located within estates. By 2023 and during the first half of 2024, this had risen to 15% of all sales. Lightstone also estimates that there are more than 6 500 gated communities and estates across South Africa. While these account for 5% of total housing stock, they account for about 15% of total housing value. While freehold properties account for the largest percentage of housing stock in SA, estates are the fastest growing sector – according to Lightstone.

Demand for estate living is growing nationwide but is particularly strong in Gauteng. Approximately half of these estate homes are in Gauteng – accounting for 16% of all sales in the province and approximately 28% of the total value of all sales. According to Lightstone, almost a third of the total value of property transactions in Gauteng in 2023 were related to estate homes. In both Gauteng and the Western Cape there has been a marked shift in estate sales from the lower price band <R1.5 million to the upper price band >R3 million, although this has been more noticeable in the Western Cape, where around a third of all homes sold in estates have been valued at more than R3 million compared to almost 28% in Gauteng. This may be partly attributable to the influx of older, more affluent semigrants to the Western Cape, many of whom opt for estate living.

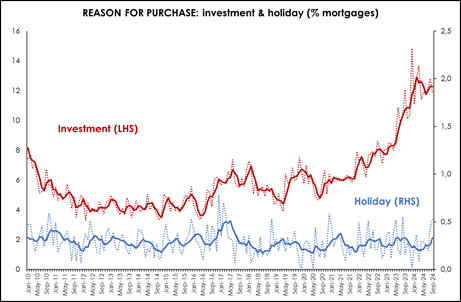

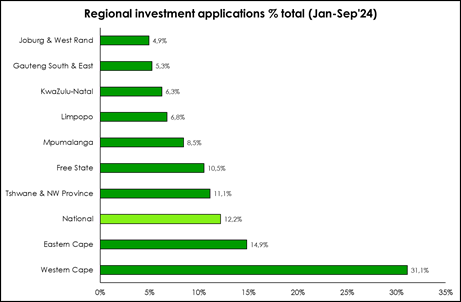

Increased demand for buy-to-let property

Source: ooba Home Loans

Since late-2021 there has been a marked increase in demand for investment properties, rising from 6.25% of applications in 2021 to a peak of 14.9% in Dec’23. The surge in investment demand has primarily been driven by the Western Cape – presumably in part the result of people planning to move or retire to the Western Cape gaining a foothold in the province before actually relocating. Alternatively, other buyers noting the robust demand for accommodation in the Western Cape have decided that an investment / buy-to-rent property is an attractive investment opportunity. In addition to the Western Cape, there has been a marked increase in investment demand in the Eastern Cape since mid-2023 and, more recently, Tshwane.

Source: ooba Home Loans

Mixed-use developments

There is a shift away from standalone homes and apartment buildings to developments which include retail, office, recreation and residential in a single building. In part this is more appealing to the property owner as it maximises the utility of the building – across sectors and over 24 hours, ie not just used during office hours and/or weekends and evenings. The appeal for such residential property owners is that they have easy access to amenities (walkability) at a fraction of the cost (time and money) than if they had to own them outright. These mixed-use developments are evident across price bands and geographically, from the conversion of former industrial sites in inner city Johannesburg to high-end luxury developments.

Growth areas

With the formation of the GNU (Government of National Unity) having been well received by financial markets, we also anticipate that any regions or districts which can be seen to have benefited from a change in governance since the May elections could potentially experience a rebound in prices and activity. While the Western Cape remains the standout performer, we have also already seen increasing activity and interest this year and during recent months in various other key metropolitan hubs and sought-after nodes around the country across all sectors, including but not limited to the high-end of the residential market.

Within the Western Cape, growth areas include the Northern Suburbs (and towns like Somerset West) and smaller towns along the West and East Coast – including the Garden Route. While the City of Cape Town remains popular, it is becoming expensive for homebuyers and waiting lists at schools are lengthy. As a result, many semigrants are instead opting to live in areas which are relatively more affordable and which have room for new homes, often in estates.

KZN has seen an increase in residential building plans passed after a period of subdued activity and is returning to the kinds of activity seen in the past. Gauteng is an area where we are starting to see some recovery in activity. Pricing is extremely attractive (particularly relative to Cape Town) and the proliferation of CIDs in areas like Sandton and Braamfontein means that security and service delivery are much improved, improving the appeal of these areas. Once service delivery (notably water) is improved, these housing markets have significant upside potential. This is the economic hub of the country so is naturally attractive to young professionals in particular, so if the lifestyle is perceived to be improving activity could rebound quickly.

Foreign buyers

Since the start of 2023, we have seen an increase in interest from and sales concluded to international buyers from a range of countries, including the UK, Germany, Zimbabwe, USA, Switzerland, Austria, UAE, France, Belgium, Sweden, Nigeria and other African countries, among others. This year we have noted an increase in interest in SA residential property – including luxury homes – among overseas buyers, including returning SA expats. and notably a steady flow of buyers from the rest of the African continent. There are certainly signs of foreigners looking to South Africa for its convenience from Europe, more relaxed lifestyle, weather and affordability, which is reinforced by the ability to work remotely. This is also particularly true of South Africans who appear to be returning to the known risks of South Africa vs the unknown risks of Europe. The certainty and stability that had made Europe appealing is now being threatened by the war in Ukraine – which is showing no signs of abating – with much depending on whether America continues to support Ukraine or not. The ongoing turmoil in the Middle East is also contributing to making SA more appealing.

That said, overseas buyers acquiring residential property in South Africa remains low overall, and in terms of volumes or number of transactions, represents approximately 5% of Pam Golding Properties’ total residential sales in SA. Areas popular among foreign buyers include the Western Cape – including Cape Town – including the Atlantic Seaboard; the Boland and Overberg regions including Franschhoek, Stellenbosch, Paarl, Hermanus; the Garden Route – including Plettenberg Bay, Knysna and George; the KwaZulu-Natal areas north of Durban, including uMhlanga and Ballito; and areas in Gauteng such as Fourways, Rosebank, Sandton, among others.

South Africans purchasing overseas

SA buyers of international property are a mix of those seeking residency and citizenship programmes – predominantly via the EU Residency Programmes, particularly those looking to secure access to the EU employment market for their children, while Mauritius and Seychelles, which are within easy reach of South Africa, are very appealing for those seeking to acquire a holiday home or permanent destination to retire to. Others are drawn to acquire investment properties in the UK in the likes of Birmingham, Leeds, Leicester, Wakefield and Manchester.

While the Portugal Golden Visa programme – which was extremely popular among South Africans seeking EU Residency, no longer supports residential property as the underpinning investment, the Greek Golden Visa programme has been very well received by our clients. We launched a student accommodation product which was eligible for this programme and the development called Arish Wonderwall in Patra, the third largest city in Greece, sold out in less than six months, and we were fortunate to ‘place’ 14 of our clients in this development. However, shortly after the sale of this development the Greek authorities changed the Golden Visa regulations, now requiring a minimum investment of €400 000 in areas with less than 3 000 inhabitants and €800 000 in areas with more than 3 000 inhabitants. A third category – that of rehabilitation projects, may still be allowed with an investment of €250 000, and in this regard, we are hopeful of launching such a development in the near future. In Mauritius, a popular primary and leisure destination for South Africans, Mont Choisy maintains its number one position as the development of choice for South Africans, while a new branded residences development in Seychelles called The Residences at Meliá Seychelles, is fast becoming the go-to for discerning buyers.

Pam Golding Properties recently extended its global reach by establishing a presence in Paris – in prime location in the heart of the 7th arrondissement, a highly sought-after, upmarket central district in France’s capital city. While marketing local residential property in this world-renowned destination, we also see the potential to bring to the Parisian market South African property, as well as other international properties marketed by Pam Golding Properties.

Outlook for 2025

The outlook for the SA economy and the residential housing market in 2025 is more positive than it has been for some time. If the early promise of the GNU is realised and more significant reforms are achieved, and greater involvement of the private sector results in a noticeable easing of logistical constraints and increased investment in infrastructure generally, some business leaders are suggesting the possibility of GDP growth rates closer to 3%. However, much will need to change to achieve growth that strong and in the interim, National Treasury continues to forecast growth of just under 2%.

The international environment remains uncertain with significant potential impacts on SAs economic outlook – for example impact on the rand, the oil price and scope for further interest rate relief in SA. The base case is for at least another 100bps in rate cuts, with inflation below target for 2025 (around 4%). This will provide significant relief for household finances and should boost demand from first-time buyers. The continued recovery in HPI at a time of subdued inflation is likely to result in sustained (if low) growth in real house prices.

Still good value

After a tough couple of years economically, the property market overall offers sound value. Areas to invest in are those where service delivery is good, either by the local municipality or if there is a strong private sector presence such as the CIDs which are popping up across the country. Buyers need to know that their investment is going to retain its value and good service delivery is crucial for that.

Ends

For further information visit www.pamgolding.co.za

Issued by Gaye de Villiers

Tel: 083 325 1939

On behalf of Pam Golding Properties

Posted by The Know - Pam Golding Properties

Housing market recovery builds momentum

Wednesday 1st of October 2025

Unchanged repo rate unlikely to stall housing market momentum

Thursday 18th of September 2025

Gauteng population growth boosts housing demand

Monday 25th of August 2025