More positive outlook for SAs residential property market in 2024

Market Overview & Outlook by Dr Andrew Golding, chief executive of the Pam Golding Property group

Tuesday 5th of December 2023

Dr Andrew Golding, chief executive of the Pam Golding Property group

Dr Andrew Golding, chief executive of the Pam Golding Property groupIn a year (2023) characterised by unusually high levels of political and economic uncertainty and volatility, central banks in most major global economies hiked interest rates aggressively in an attempt to contain renewed inflationary pressures caused initially by the 2020 pandemic but reinforced by the subsequent conflict in Ukraine and the Middle East, which disrupted global trade and commodity prices.

South Africa was not spared and the Reserve Bank responded with an aggressive 475 basis points of interest rate hikes starting in late-2021, more than fully reversing the rate cuts during the pandemic, which then triggered a boom in housing market activity, further fuelled by pent-up demand. The resurgence in the oil price amidst the global turmoil, coupled with a weaker rand, created higher petrol and diesel prices, which further strained households’ already pressured finances.

While the global outlook for 2024 remains uncertain – particularly as the conflict in Ukraine and the Middle East continues – there is good news on the inflation and interest rate front. The inflation rate in Europe and the USA has peaked and, as a result, the upward phase of the global interest rate cycle appears to have ended. While the timing of likely interest rate cuts in the new year is far from certain, there is widespread consensus that the next move in global interest rates will be a reduction, which will create room for local interest rates to begin declining once more.

In South Africa, it appears that interest rates have finally peaked, with the MPC keeping interest rates unchanged at their final meeting of the year. This was the third consecutive meeting at which interest rates remained unchanged, however, it was tempered by a hawkish statement which warned that they would hike rates further if necessary.

Against the backdrop of a subdued economic growth rate, with household finances under pressure from a rising cost of living and a series of interest rate hikes, it was no surprise that activity levels in the local housing market slowed during 2023.

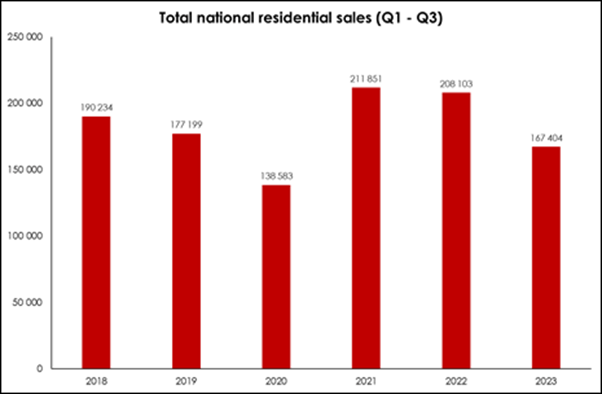

According to Lightstone, total sales volume (units) during the first three quarters of the year totalled 167 404 transactions, which is nearly 20% below the still elevated total sales during the same period in 2022 but also 5.5% below the same period in 2019 (see chart below).

Source: Lightstone

Luxury Market

In contrast to this overall picture, however, in the high-end, luxury residential market in the R25 million+ price range, Pam Golding Properties achieved a 30% increase in unit sales over the previous year, with sales of homes upwards of R80 million and beyond. Furthermore and in line with the Western Cape market’s general appeal and within the Cape Metropole, the Pam Golding Property group concluded significant top-end sales, including: a R90 million transaction and a R56.5 million sale in Bishopscourt, as well as two bungalows in Clifton at over R30 million each, and other top-end houses and luxury apartments sold in Camps Bay and Clifton, with a buoyant luxury market in Constantia, Bishopscourt and surrounding areas, with numerous sales in the R20 million to R40 million price band. Currently, Pam Golding Properties is marketing a luxurious five-bedroom house in Clifton at R170 million.

In addition, certain other coastal areas have also followed this trend. In Hermanus, for example, Pam Golding Properties achieved a record price of R43 million for the area and another record price of R24 million for a beachfront property in Betty’s Bay, while in the George and Mossel Bay region noteworthy sales include R24 million for a home in Fancourt, R23.5 million for a Wilderness Coastal smallholding, and R22 million for a home in Gondwana Game Reserve. In Beacon Bay in East London, the highest residential sale for R9.8 million for a luxury family home was also concluded. Further up the coast and indicating the perceived value of oceanfront property we concluded a sale of R8 million in Port Shepstone, in one of the best surfing and rock fishing spots on the KZN South Coast.

Then perhaps surprisingly, and as an indication of what we believe is the early signs of the resurgence of the Johannesburg market, we are experiencing an increase in enquiries for luxury homes in areas such as Sandhurst, Westcliff and Bryanston with numerous sales in excess of R20 million concluded. A highlight in this regard was a successfully concluded sale of R54 million in Waterfall Equestrian Estate in Midrand. A noticeable trend which augurs well for the market is in the suburb of Houghton where older properties are being acquired, consolidated and redeveloped into luxury clusters or high-end sectional title units. Locations offering prestige, top-notch security and a luxurious lifestyle are in high demand.

Increase in Tourism & International Buyers

Furthermore, and encouragingly, we are seeing a significant increase in tourists to the Cape, with the well-managed Cape Metro also benefiting from a surge in semigration from various regions generally to the north of the country. In addition, international upheaval has paradoxically made the Cape an interesting proposition for numerous international buyers. Market sentiment is positive and prospective buyers are enjoying the unique and diverse lifestyle on offer, from the sandy white beaches of the Atlantic Seaboard with its vibrant V&A Waterfront to the vineyards and tranquillity of the Southern Suburbs.

Not surprisingly, with its high global profile, and very appealing lifestyle amid the beauty of its natural surrounds, Cape Town has already seen an influx of international buyers active in the market – not only in the top end of the market, but across all price ranges, demonstrating confidence in the Mother City’s residential property market.

South Africa offers exceptional value for money – in the world-class city of Cape Town, for example, USD1 million will enable you to acquire a residential property of approximately 200sqm, while the same price tag will only secure 33sqm in New York, 34sqm in London, 43sqm in Paris, 44sqm in Sydney and just 17sqm in Monaco.

Most international buyers concur, commenting that the value offered by properties is significant and the lifestyle on offer in South Africa compelling, ranking with the best on offer elsewhere in the world. This segment of the market also remains relatively unaffected by interest rate hikes. Buyers with significant resources are also keen to diversify their investments while at the same time benefiting from living in properties offering outstanding views, lifestyle and amenities, which are in abundance.

Pam Golding Properties’ residential property sales to international buyers in the last 12 months comprised 5.4% of our total sales, concluded with purchasers from around the globe with the top 16 being the UK, Germany, Zimbabwe, USA, Netherlands, Belgium, Nigeria, Canada, Switzerland, Angola, Botswana, China, Italy, Congo, France and Lesotho. Their locations of choice vary considerably, including the Cape Atlantic Seaboard, Cape Winelands, Whale Route, the Garden Route towns of George, Knysna and Mossel Bay, and St Francis Bay and Port Alfred in the Eastern Cape, Hoedspruit, Nkomazi, Fourways in Johannesburg, and Underberg, among many others.

House Price Inflation

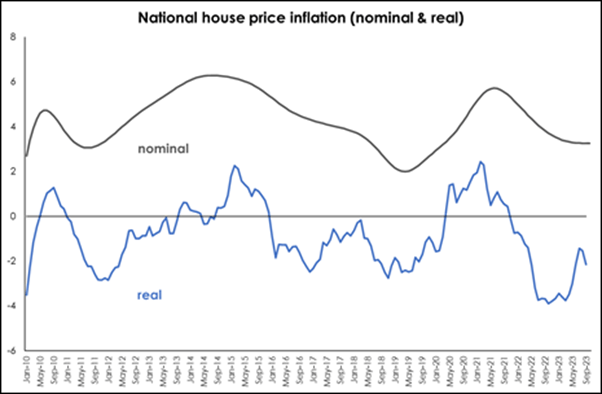

While the national house price inflation rate, as measured by the Pam Golding Residential Property Index, has shown clear signs of stabilisation in recent months, the soaring inflation rate took its toll on growth in real prices (see chart below). Now however, with inflation being brought back under control – returning to the Reserve Bank’s inflation target and likely easing towards the mid-point of 4.5% by year-end, the outlook for real national house price inflation is markedly more positive in 2024.

SOURCE: Pam Golding Residential Property Index & Statistics SA

Regional Markets

| House price inflation ave | 2020 | 2021 | 2022 | 2023 ytd

(Jan – Oct’23) |

| Gauteng | 2.91 | 4.46 | 2.56 | 1.61 |

| Western Cape | 4.53 | 6.63 | 6.26 | 5.57 |

| KwaZulu-Natal | 4.07 | 5.35 | 4.33 | 2.28 |

| South Africa | 3.82 | 5.48 | 4.18 | 3.31 |

SOURCE: Pam Golding Residential Property Index

The Western Cape housing market has registered the strongest growth among the three major regions during the past four years, including the year to date, with KZN following in second spot.

Metro markets

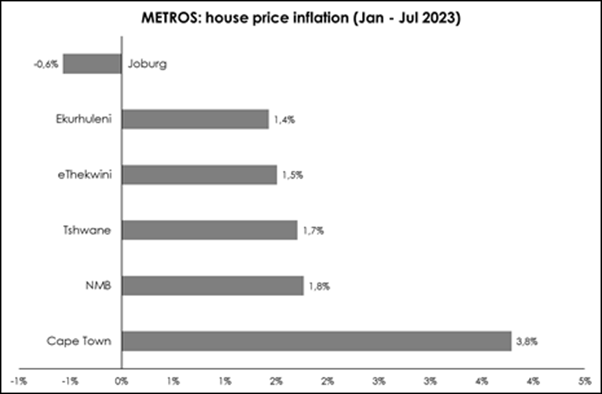

House price inflation in all major metro housing markets is losing momentum, with the exception of Cape Town where growth in prices stabilised at 3.8% in recent months. Johannesburg is the only major metro where prices are declining from year-earlier levels, being in negative territory since January 2023 (latest data is July 2023).

SOURCE: Lightstone

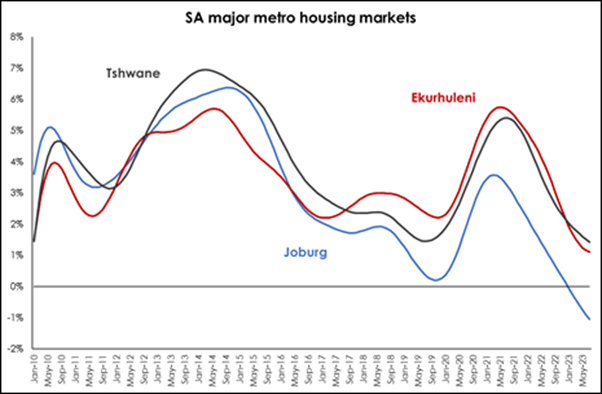

Within Gauteng, all three sub-regions are experiencing slowing growth in house prices with only Johannesburg recording year-on-year declines (see chart below).

SOURCE: Lightstone

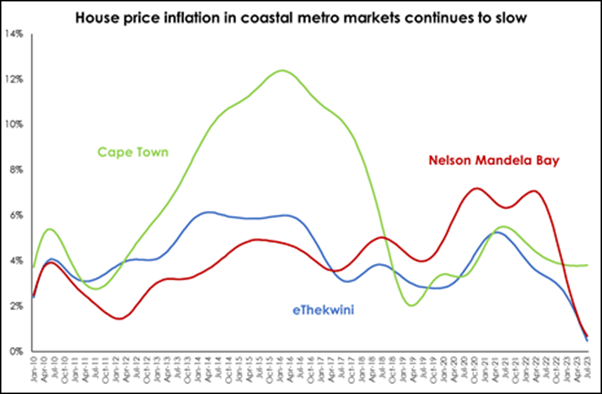

Within the coastal metros, a period of outperformance by Nelson Mandela Bay has now ended, while Cape Town is currently the top performing among the three major coastal metros (see chart below).

SOURCE: Lightstone

Market trends

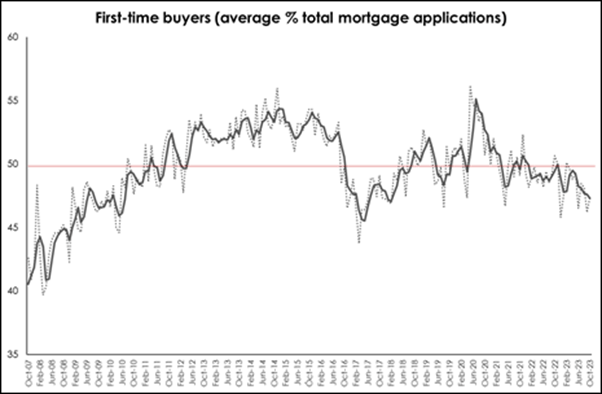

Interestingly, according to ooba, the average age of bond applicants rose to 40 years in October 2023, for the second time this year, while the average age of interest rate-sensitive first-time buyer bond applicants remained elevated at 36 years.

SOURCE: ooba Home Loans

First-time buyers are typically more sensitive to a rising interest rate environment as they are at the early stages of their careers and have fewer financial resources for deposits and associated costs of home ownership. As a result, after stabilising just below 50% in the wake of the post-Covid boom, the percentage of applications received from first-time buyers continues to weaken, averaging just 47.3% in the three months to October 2023. However, with interest rates stabilising and expected to embark on a downward trajectory, and with sound value to be had in the marketplace, the potential exists for first-time buyers to capitalise on opportunities to gain a foothold in the property market.

Encouragingly, measures of banks’ appetite for lending to the market include:

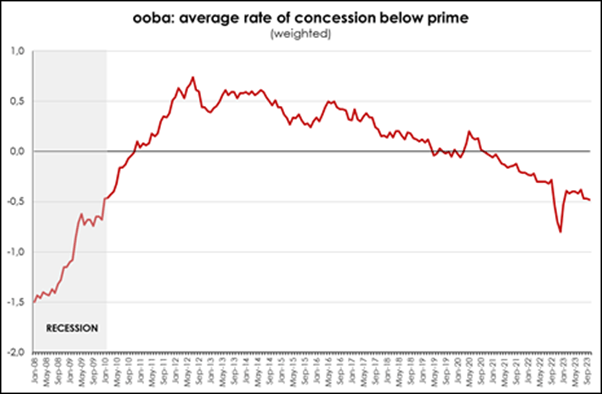

- Competitive pricing of loans – after a sharp adjustment between Oct’22 and Jan’23, ooba’s average (weighted) concession below prime continued to improve during the course of the year – declining from -0.39% on Feb’23 to -0.48% in Oct’23. This is the most competitive pricing seen since the final years of the 2008/09 recession in the wake of the global financial crisis and goes some way towards making home loans more accessible for South African home buyers.

SOURCE: ooba Home Loans

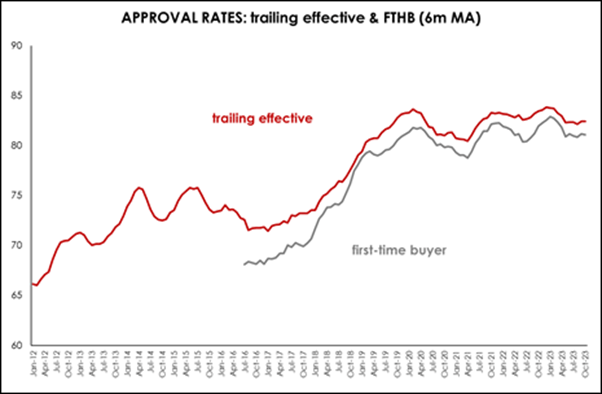

- Approval rate – approval rates have declined somewhat in recent months but remain elevated, reflecting the ongoing appetite of banks to extend mortgages. Buyers whose applications have been pre-qualified continue to enjoy a significantly higher approval rate compared to applications not linked to pre-qualification.

SOURCE: ooba Home Loans

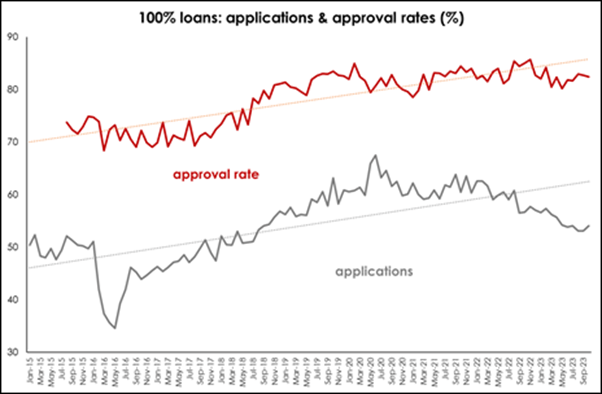

- Applications for 100% loans surged in the wake of the interest rate cuts in the initial stages of the pandemic – (reaching 67.5% of applications in June 2020), but have since drifted lower (54.1% in Oct’23), particularly as the Reserve Bank continued to raise interest rates from late-2021 onwards. In contrast, the approval rate for 100% loan applications remains elevated. In 2019 (before the pandemic) the approval rate for 100% loan applications was 81.7%, while during the first 10 months of 2023, approval rates averaged 82.1%, on a broadly similar level.

SOURCE: ooba Home Loans

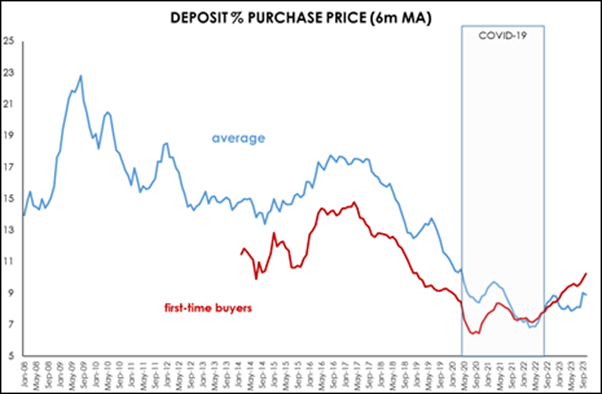

- Deposits – one indicator which does appear to have shifted is deposits as a percentage of purchasing price, particularly deposits paid by first-time buyers (FTB). After reaching a low of 6.5% of purchase price in Oct-2020, deposits paid by FTB have since risen to 10.3% in 2023 – a level last recorded in Jan’19. Average deposits (both FTB and repeat buyers) reached a low of 7.2% in Jan’22 and have since risen to 8.95% in Oct’23. Prior to the pandemic, FTB typically paid a smaller deposit as a percentage of purchase price than repeat buyers but since the pandemic, they pay more. Either way, the increase in deposits suggests that banks are becoming a little more cautious in extending credit.

SOURCE: ooba Home Loans

Other Key Trends

Demand for Sectional Title : The surge in demand for freehold properties fuelled by the pandemic – as the ability to work from home prompted many homeowners to shift from smaller, ST properties in business nodes, to larger FH properties in peripheral suburbs of the metro areas or smaller towns – appears to have somewhat faded and the desire for sectional title has resumed. This could be attributable to the return to working in the office and/or SA’s young population buying a home for the first time ie affordability. Furthermore, changing lifestyles means that people increasingly prefer lock-up-and-go living and better security and lower maintenance of ST living.

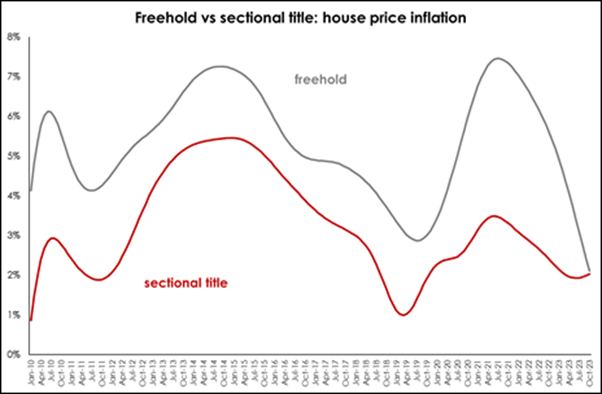

In October 2023, growth in freehold prices had slowed to 2.11% compared to 2.03% for sectional title homes. While growth in FH prices continues to lose momentum, house price inflation for ST properties appears to be showing tentative signs of recovery.

SOURCE: Lightstone

SOURCE: Lightstone

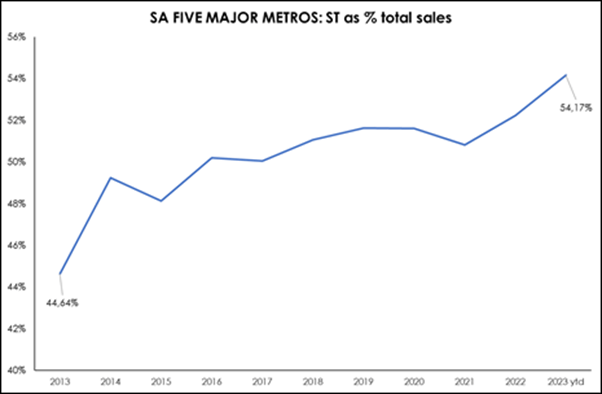

Increased demand for ST homes is also evident when looking at the homes sold in the five largest metro markets. A decade ago, less than 45% of all homes sold were ST but during the year to date, nearly 55% of homes sold were ST – highlighting the growing preference for ST homes. The bulk of new developments in major metro areas are typically residential blocks, with a growing percentage of mixed-use developments. Sales of ST range from a high of 63.1% of total sales so far this year in Tshwane to just 45.1% in Johannesburg.

Ongoing Semigration

Despite a reduction in sales volumes in the market country-wide, mainly driven by the current economic headwinds that the country is experiencing and certainly driven by the recent rise in interest rates, there continues to be significant buyer interest in the greater Western Cape market – including the Boland & Overberg regions and Garden Route, as well as KwaZulu-Natal and Eastern Cape coastal regions. Positively, Gauteng does still attract a large portion of first-time buyers and semigrators who are drawn by the employment opportunities and who are able to gain a foothold in the market due to the relative affordability of homes.

No property market keeps going in one direction only but what we are seeing is the increase in popularity of new, previously less fashionable areas (for permanent residences) in the Western Cape, Boland and Overberg and Garden Route areas. Examples of this would be smaller towns and areas such as Worcester, Langebaan and Paternoster up the West Coast and hamlets like Greyton and Riebeek Kasteel.

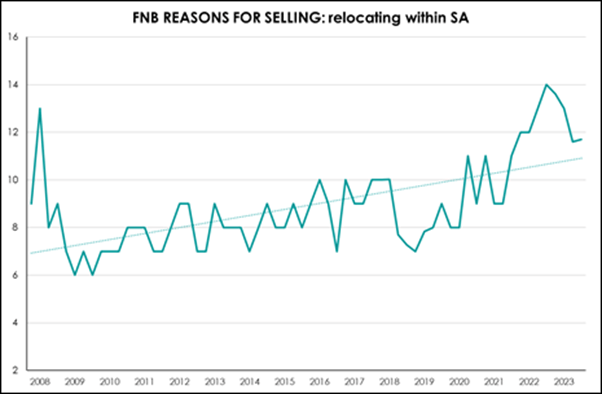

SOURCE: FNB Estate Agent Survey

According to the Q3 2023 FNB Estate Agent Survey, 12% of homes sold in Q3 were due to homeowners relocating within South Africa – an indicator of ongoing semigration or movement between provinces – although this has slowed as a percentage of total sales as rising interest rates made it more expensive to purchase a new home.

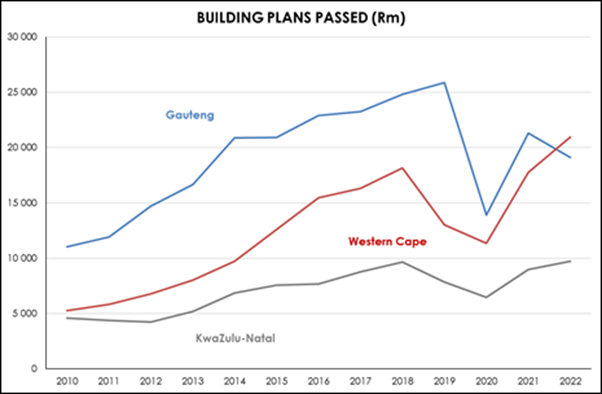

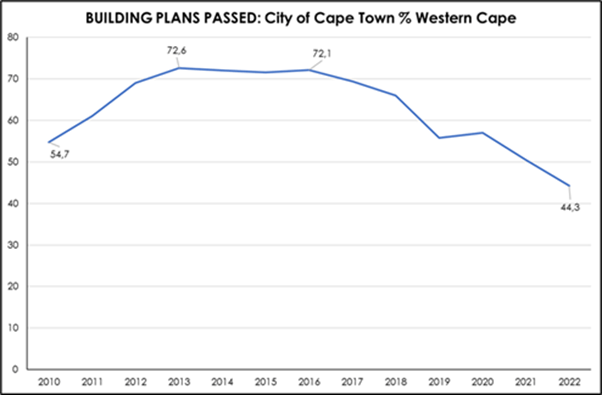

The impact of semigration is also evident in the changes in patterns of building plans passed. Data from StatsSA shows that in 2022, the value and number of building plans passed in the Western Cape exceeded those in Gauteng for the first time on record.

Building plans passed reflect the impact of semigration and the shift to ST

SOURCE: Statistics SA

SOURCE: Statistics SA

Given the shortage of vacant land for developments, a growing percentage of these new building plans are being passed for areas outside the Cape Town metro area, with Knysna and the Garden Route in general the primary beneficiaries of this trend.

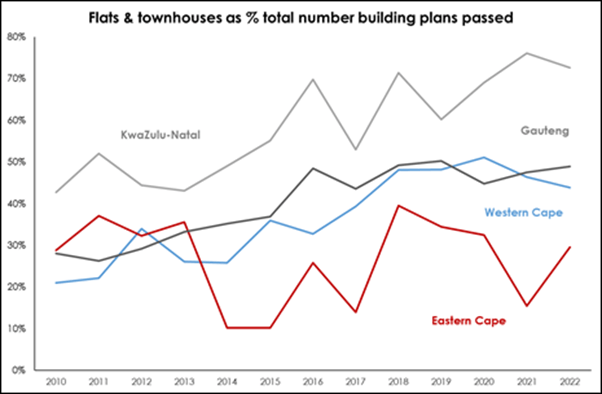

Notably, a growing percentage of these building plans passed are for ST homes (see chart below).

Source: Statistics SA

Rental Market

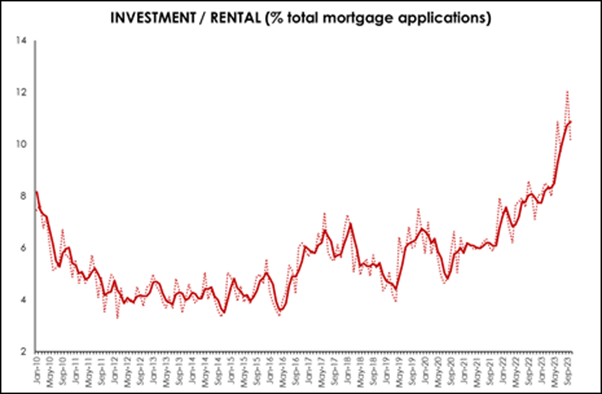

There has been a marked increase in applications for investment or buy-to-rent properties in recent months, according to ooba. This suggests that buyers see the residential property market as an attractive investment proposition, and could also include those who ultimately intend to semigrate elsewhere in the country, opting to gain a foothold in their desired town or metro housing market with an investment or rental property until they are ready to relocate.

This surge in demand for investment properties is being primarily driven by the Western Cape, where investment applications have risen to 28.1% of all applications received in October 2023. In Cape Town, tenant activity and demand has increased, resulting in a significant under-supply of available homes to rent. The combination of semigration, excellent service delivery and favourable climate has led to a substantial increase in the number of tenants seeking rental properties. In particular, the City Bowl, Atlantic Seaboard and Southern Suburbs have become highly sought-after areas, resulting in fierce competition for rental properties. As a result, Cape Town has experienced healthy rental escalations. Currently, the vacancy rate is just 3.62%, the lowest it has been since the start of the pandemic.

SOURCE: ooba Home Loans

Multi-generational / shared living:

As affordability remains a concern for both young and senior citizens, coupled with a desire for company and a sense of community, the trend towards multi-generational and shared living continues.

Outlook for 2024

As is always the case, within the slowing overall activity levels there are vast differences between the pricing, demand and activity in different towns, suburbs and property types driven by local demographics and lifestyle trends.

Further complicating the outlook in 2024 is the prospect of US and South Africa’s elections next year, although the recent decision by S&P Global to affirm SA’s credit rating is a reassuring sign of stability.

Generally speaking, the outlook for next year is likely to show an improvement in a number of key residential property metrics when compared to 2023. Dominating this improvement in outlook will hopefully be the start of a downward trend in interest rates which nearly always signals an uptick in activity and which, as a consequence, is also likely to herald the start of a cycle of real house price growth.

Furthermore, with the toll that loadshedding took on the economy in 2023 hopefully expected to ease significantly during the course of next year, prospects for growth should improve.

We also anticipate a continued divergence between the performance of different regional and metro housing markets – reflecting both the stability of the local municipality, the affordability of homes, the strength of the local economy and the lifestyle offering of the town/suburb. This will make location an increasingly important factor.

In 2024 agility will be key – as it was during the pandemic – which is likely to result in the residential property market (much like other sectors of the property market) being forced to be as flexible as possible. For example, new residential developments which offer units for purchase as well as short and long-term rentals (with aparthotel facilities), and mixed-use which allows for commercial and residential in a single new development.

The shift to ‘green’ homes will become more mainstream. While loadshedding may ease, the rising cost of electricity (coupled with some measure of loadshedding) is likely to make the shift to solar appealing for those who can afford it. The continued breakdown in municipal services – not only due to poor maintenance but also increased urbanisation/semigration, placing greater pressure on limited infrastructure – will make going off-grid or at least increasing self-sufficiency an increasingly appealing option.

While the latest semigration wave was triggered by the pandemic, ie work from home, it is now being driven by lifestyle and governance factors. The shift to low-maintenance, convenient sectional title properties, given considerations of security and cost, will continue, particularly in the major metropolitan areas and key commercial hubs, and developers are responding to this demand for sectional title living, with new flats and townhouses increasing.

Globally, Savills researchers from around the world are predicting a more positive real estate investment environment in 2024, with 57% on average expecting a moderate to strong increase in investment activity next year, although this rises to as high as 70% of respondents for multifamily residential property – a sector where demand outstrips supply in many areas.

Offshore property

While Portugal’s Golden Visa programme, as we know it, has come to an end, the programme remains open for those wanting to invest in non-real estate qualifying Private Equity Funds. However, the investment amount is now back to €500 000, where it was when the programme was launched. Furthermore, the approval process is taking longer with new applicants now waiting for about 2.5 years before being able to undertake biometrics, which is the final hurdle before applications can be processed.

Although we have, for the time being, ceased to offer the Portugal Golden Visa programme, we continue to monitor the developments that clients have invested in and have met with the Portuguese Ambassador in South Africa, to try to facilitate the approval process. Going forward a new entity called Agency for Immigration, Migration and Asylum (AIMA), will handle the Golden Visa applications, which should improve the situation.

Having formed an agreement with the Latitude Group, one of the world’s largest citizenship and residency advisory groups, operating in over 20 countries, we are now marketing an exciting commercial real estate opportunity in Barcelona and Madrid in Spain , which offers European Residency via the Spanish Golden Visa programme. The programme requires a €500 000 investment in real estate, however, they offer an immediate 10-year leaseback at €150 000, which means the investment is effectively €350 000. The benefit of the programme is that EU Residency is achieved in under six months, allowing the main investor and his or her immediate family to live and study in Spain, less than six months after making the investment. EU Residency also allows travel throughout Schengen Europe without requiring a visa.

Furthermore, we have just launched our first investment opportunity into the Greek Golden Visa programme. Working with Arish Capital, whom we have worked with extensively in Portugal, we launched a new development in Patra, Greece’s third largest city. The development will consist of student accommodation, servicing the 35 000 students that attend three large universities in this city. The development provides for a fixed annual return of 5% on capital invested for the first five years – and also serves as the supporting investment to gain access to their GV programme. The Greek Golden Visa can be obtained in less than six months allowing investors to live in Greece and provides visa free travel throughout Schengen Europe. The requisite investment for the Greek Golden Visa programme is €250 000, making it the most affordable way to acquire EU Residency.

All comments above by Dr Andrew Golding, chief executive of the Pam Golding Property group

For further information visit www.pamgolding.co.za

Posted by The Know - Pam Golding Properties

A significant moment for housing market as interest rates drop

Thursday 19th of September 2024

Scams Affecting Rental Properties: What to Know and Do

Thursday 12th of September 2024

Cape Town ranked 17th on Savills’ global Executive Nomad Index

Thursday 29th of August 2024