By Dr Andrew Golding, Chief Executive

Signs that the residential property market is beginning to stabilise

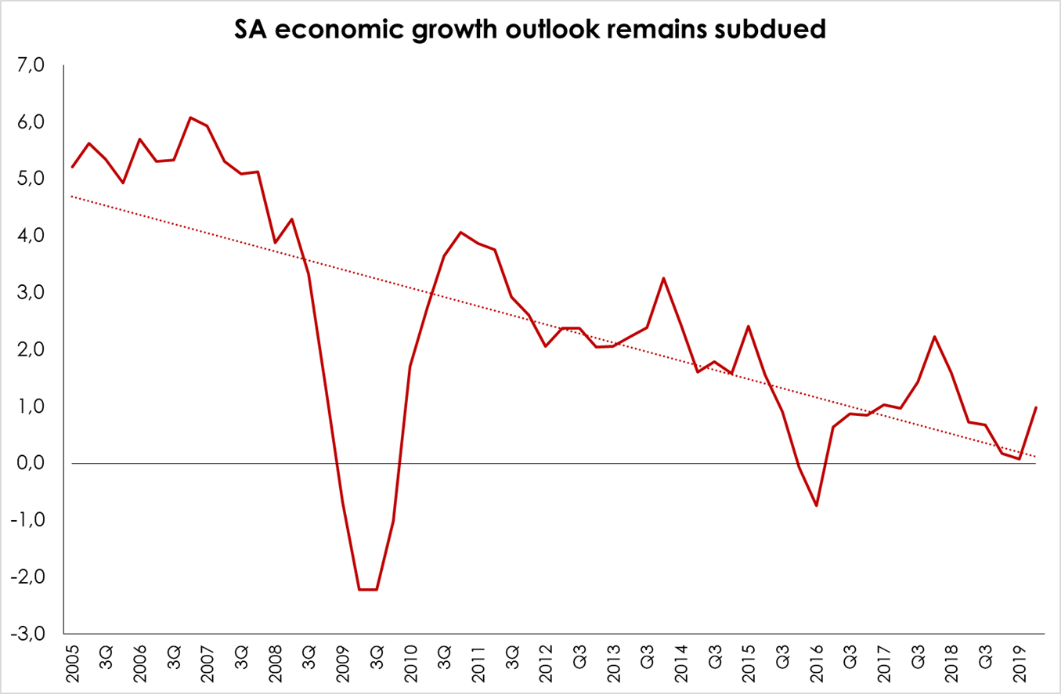

Overall, 2019 is proving to be another year of tepid economic growth (see chart below), resulting in yet another year in which government revenues have disappointed – placing additional pressure on the country’s financial situation and in turn, on consumers.

SOURCE: SA Reserve Bank

SARB GDP growth forecast 2019 = 0.6%, 2020 = 1.5% and 2021 = 1.8%

Until there is greater clarity on the prospects of a recovery in the local economy, the housing market, which remains resilient but is currently weighted in favour of buyers, is unlikely to enter another fully-fledged recovery. The recent recurrence of load shedding, ongoing socio-political challenges and a volatile global environment have created further headwinds.

It is also important to keep in mind that the ongoing turmoil created by Brexit, the brewing trade war between China and the US and the downturn spreading across Europe is raising the very real threat of a global recession. It was recently noted that the Wall Street Journal’s uncertainty index rose to a record high in August. This suggests that financial markets are currently more uncertain than was the case after 9/11, the European debt crisis and Trump’s election. Current estimates suggest that there is a 30% probability of a global recession.

Notably, Professor Francois Viruly (UCT), recently pointed out that it is not the depth of the slowdown that is hurting the property market this time but rather the length of time the economy has remained sluggish. Continued pressure on consumer household finances, and on property developers, is creating a robust headwind for the market.

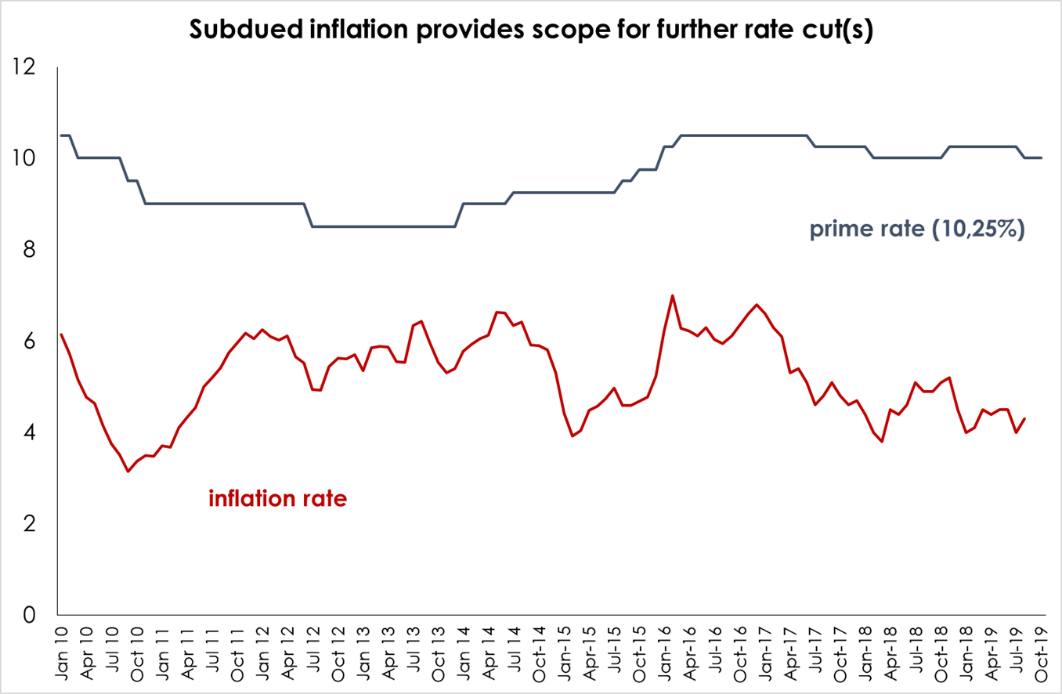

However, there is one upside to this sustained period of weak growth. Price pressures from higher global oil prices and/or Rand weakness are having limited impact on the inflation rate, which is stabilising around the mid-point of the inflation target range (3-6%). This means that there is little pressure on the Reserve Bank to raise interest rates. There is even a small chance of a further 0.25 bps rate cut in November this year or in early 2020, but other than that, interest rates are expected to remain steady for an extended period of time.

SOURCE: SA Reserve Bank and Statistics SA

SARB inflation forecast 2019 = 4.2% and 2020 = 5.1%

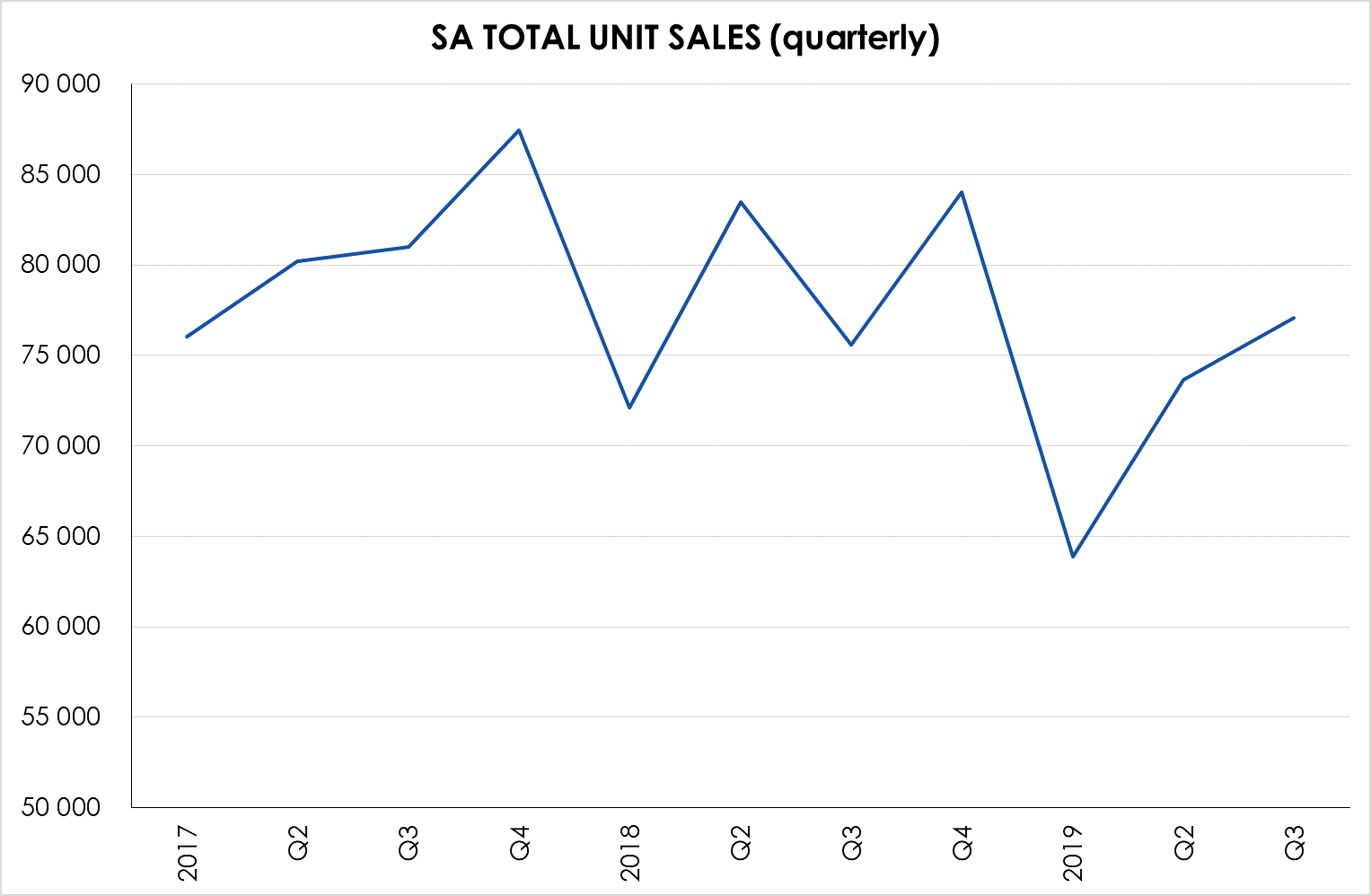

Sales volumes up since Q1 2019

According to Lightstone, although total unit sales slumped in the first quarter 2019 (quite possibly due to load shedding and pre-election jitters) they have since rebounded strongly. Further good news is that conditions in the national property market are, nonetheless, beginning to stabilise. From a low in Q1 2019, unit sales have since risen steadily from 63 887 in Q1 to 73 656 in Q2 to 77 086 in Q3. And unit sales during the first half of 2019 remain just over 11% below year-earlier levels, Q3 2019 sales are 2% above year earlier levels (i.e. above Q3 2018).

The increase in units sold is seen partially as a result of growing competition between financial institutions for market share, resulting in the easing of lending conditions with loans – including 100% loans – being extended at a pace last seen 12 years ago, and generally lower deposits required.

SOURCE: Lightstone

One of the signs of banks’ increased appetite for bank lending is the fact that mortgage advances are growing at a faster pace than house prices (see chart below), suggesting that there are more home loans than before – a scenario last seen in 2012. According to ooba, the average interest rate achieved for its buyers in Q3 2019 was 16 bps lower than in Q3 2018.

This appetite for lending, combined with relatively low interest rates plus inflation which has surprised on the downside in recent months, reinforces the likelihood that conditions could stabilise. However, for a more sustained recovery in the market, it will require an improvement in economic growth and employment prospects.

Market activity

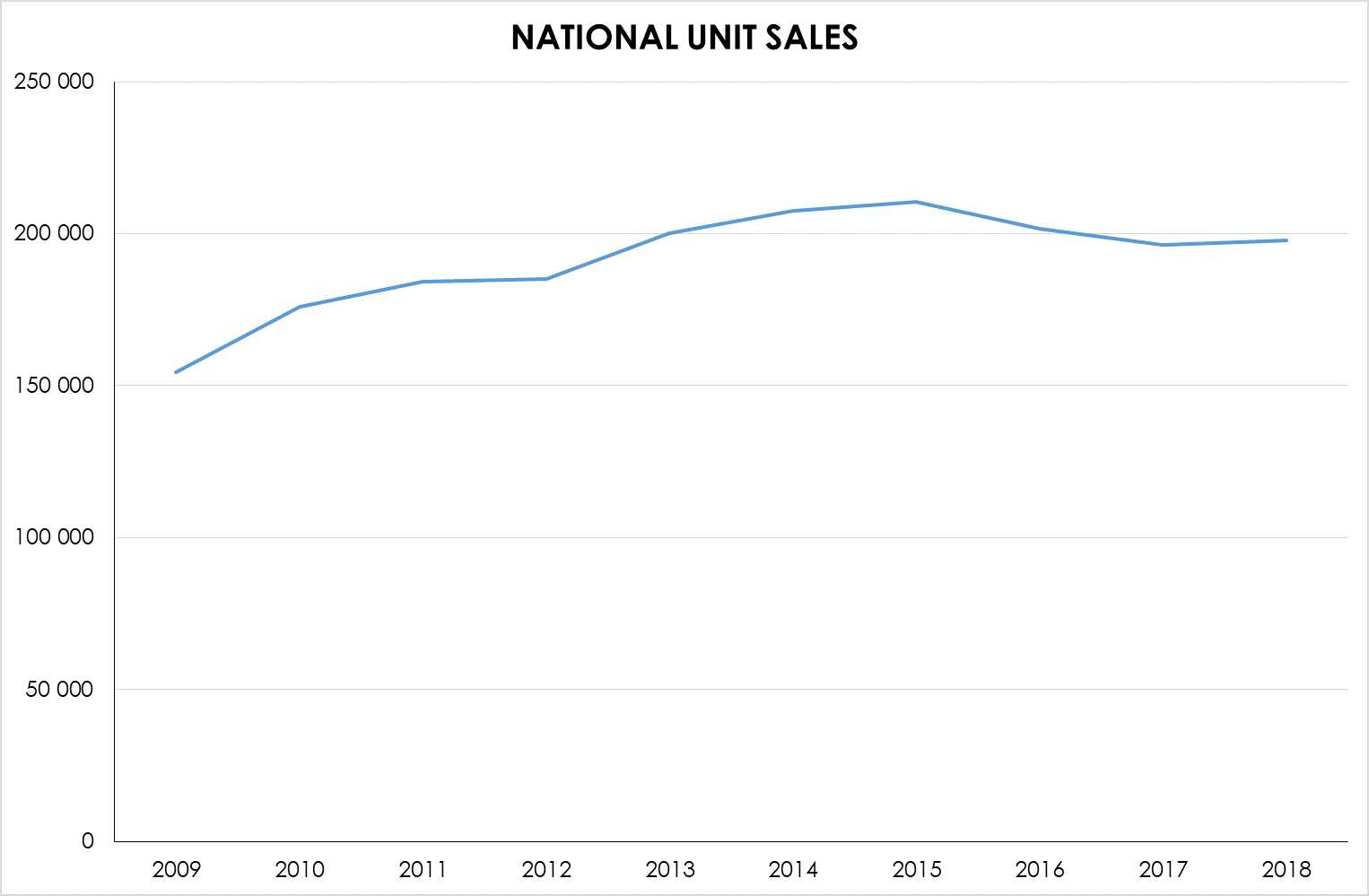

However, this is seen against a backdrop which reveals that total housing activity slowed from a peak of 210 465 units sold in 2015 to 196 375 units in 2017 before rebounding modestly in 2018. Sales last year totalled 197 634 units – nearly 13 000 units or 6.1% below the 2015 peak.

SOURCE: Lightstone

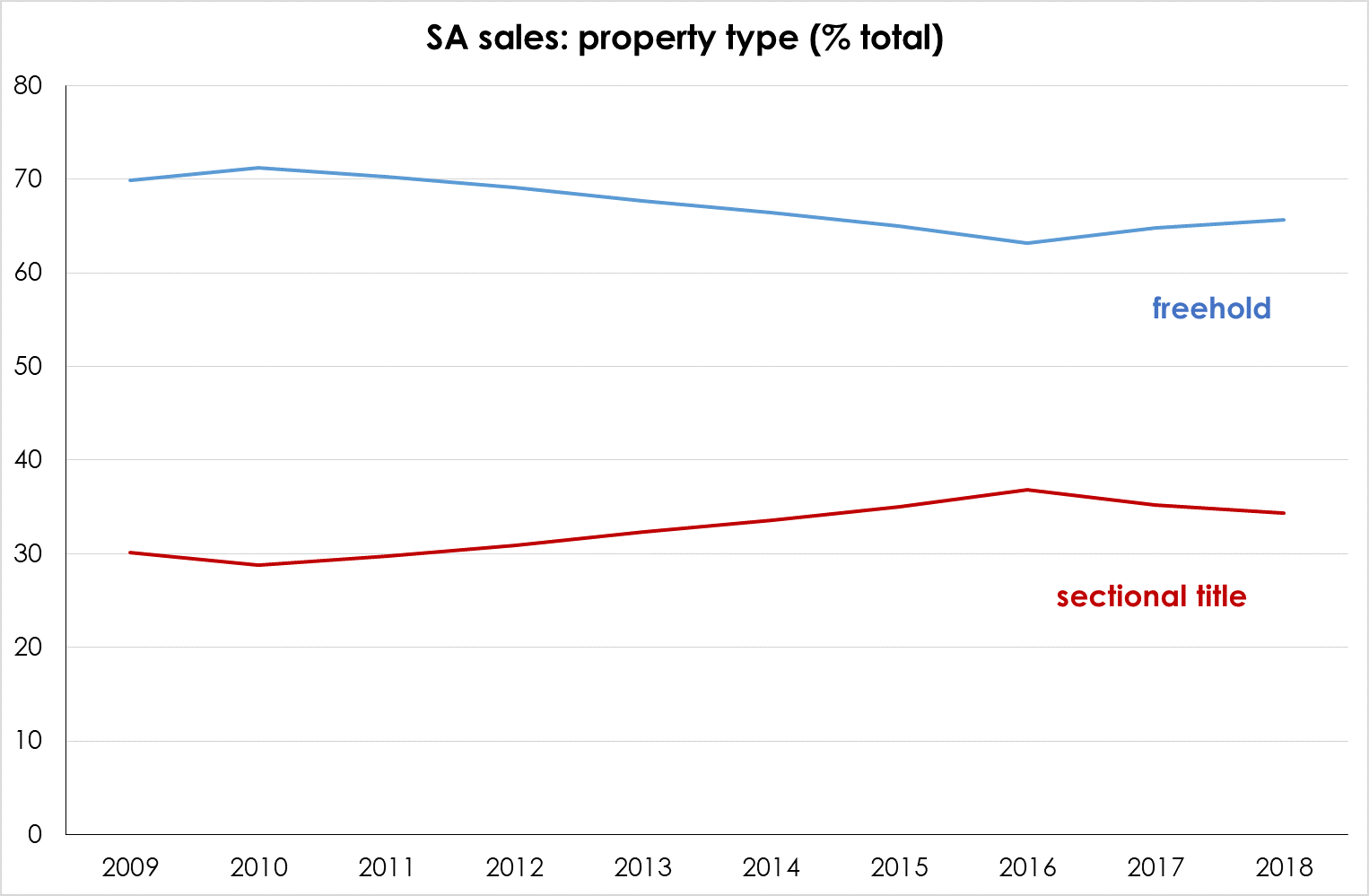

Of interest is the shift from freehold to sectional title which is evident in the national sales, with freehold properties accounting for 71.2% of all sales in 2010 – declining to 63.1% in 2016 before rising to 65.7% in 2018. (As affordable housing is typically freehold, the shift to sectional title homes is likely to be more evident if one were to exclude affordable housing).

SOURCE: Lightstone

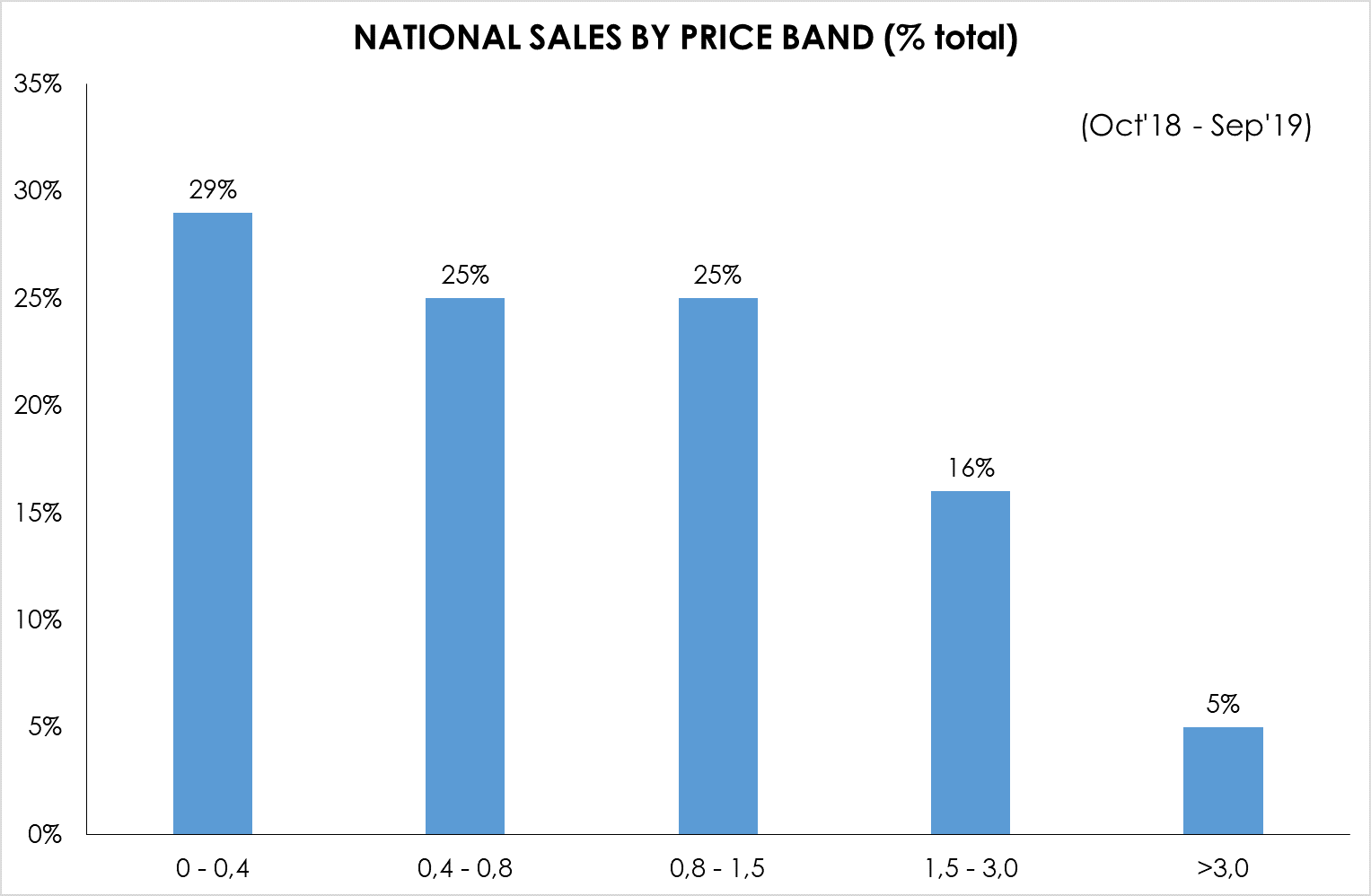

According to Lightstone, nearly a third (29%) of all sales across South Africa during the past 12 months (Oct’18 – Sep’19) were in the lowest price band (<R0.4m) while just 16% were between R1.5-R3m and only 5% of all sales during this period was properties priced over R3m. Nearly 80% of all properties sold during the past 12 months were priced below R1.5 million.

According to FNB, despite the slowdown in sales volumes, the middle income categories continue to see growth in unit sales from year-earlier levels while the lower and the upper ends continue to contract. The decline in lower end sales can be attributed to a deterioration in affordability high levels of unemployment, while the upper end is presumably impacted by a loss of confidence and the fact that many sellers can afford to sit out the market down-cycle.

SOURCE: Lightstone

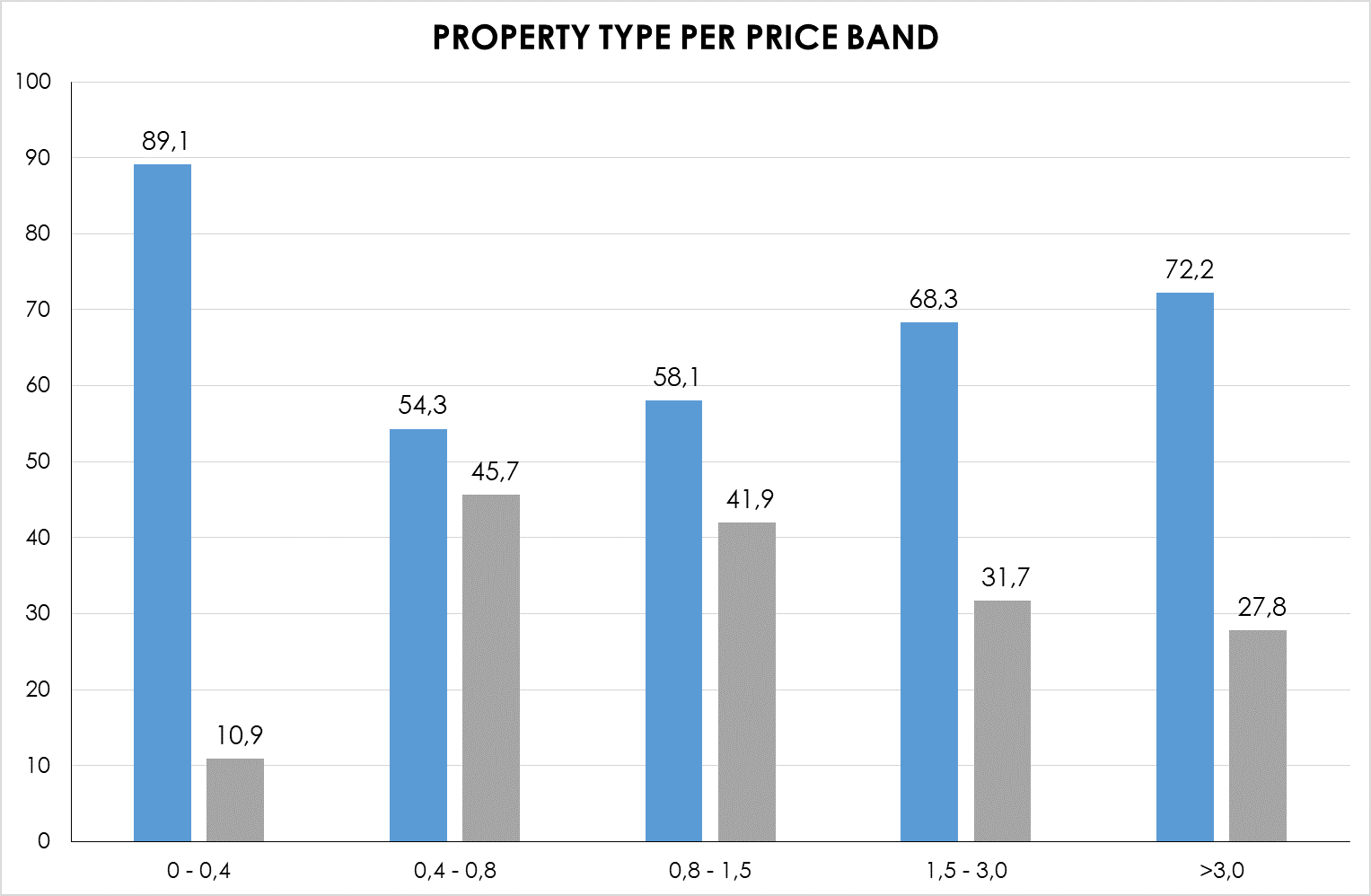

During the past 12 months (Oct’18-Sep’19), freehold sales have dominated in all price bands – particularly in the <R400 000 category (largely affordable housing) and in the upper price bands (notably >R3m). Sectional title properties account for almost half all sales in the R0.4 – R0.8m and just over 40% in the R0.8 – R1.5m price band.

Interestingly, over the past 12 months (to Sept ‘19), just 9.9% of all sales have been of new properties. And during this period, just over 35 000 vacant plots have been sold – nearly 20% of which (19.4%) were located within security estates. Of all homes sold, 13.5% were located in estates, and of all new homes sold, almost 10% were located in estates.

Price performance freehold vs sectional title

| South Africa | Average price (Rm, 2019) | Five years % (2014-2019) | Ten years % (2009 – 2019) |

| -freehold | 1.12 | +18.8 | +85.8 |

| -sectional title | 1.03 | +24.2 | +51.4 |

Further to the above, during this 12 month period to September 2019, the average price of a sectional title property sold was R1.07m, while the average price of a freehold property was R1.15m (these differ from the figures in the table above because the figures in the table do not separate out estate homes and are for the year to date rather than the past 12 months).

For the same 12-month period, the average price of an estate home sold was R2.08m – nearly double the average price of a freehold home (although this figure will have been influenced by a large percentage of affordable freehold properties coming on to the market).

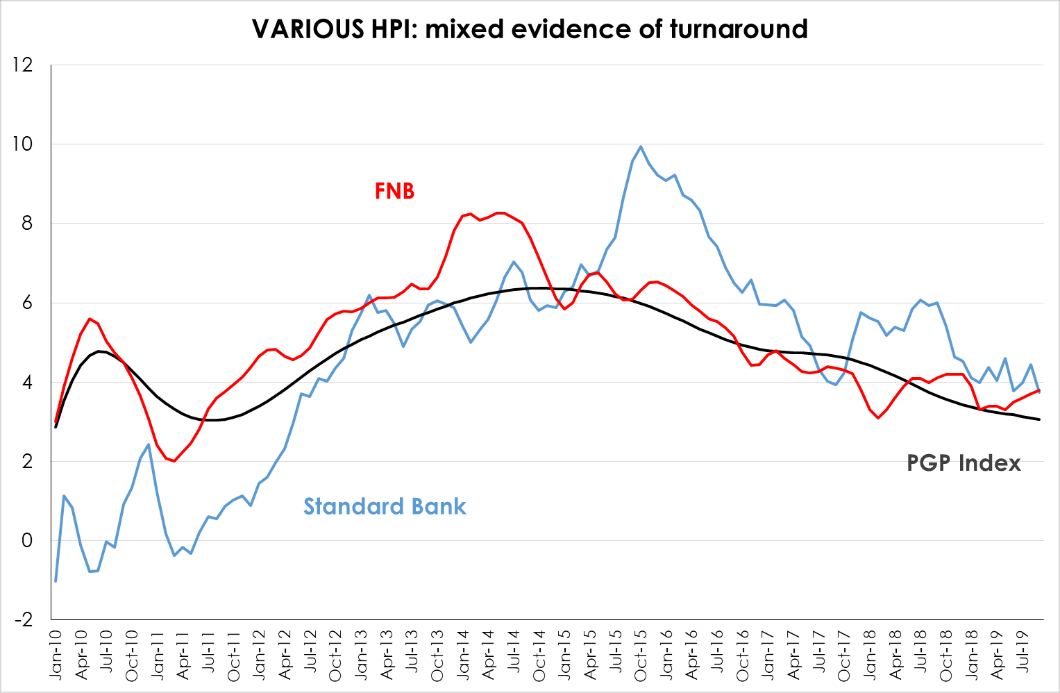

According to the Pam Golding Residential Property Index, house price inflation continues to slow.

SOURCE: Pam Golding Residential Property Index

While the Standard Bank and PGP House Price Indexes continue to slow, the FNB index has rebounded somewhat in recent months. During the year to date (September), the PGP Index has averaged 3.21%, FNB = 3.54% and Standard Bank = 4.12%.

SOURCE: Pam Golding Residential Property Index

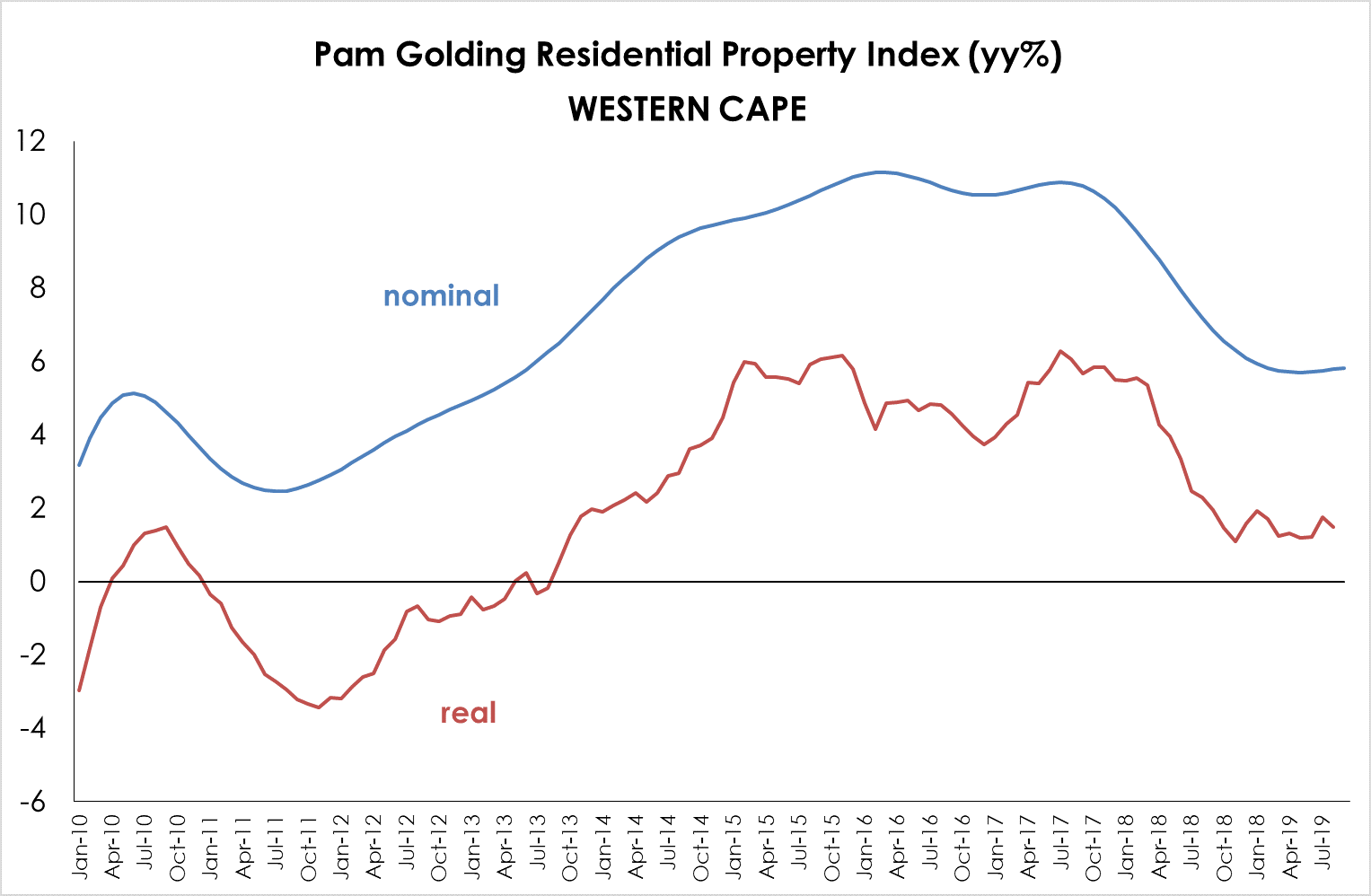

Even as inflation surprises on the downside, the continued slowing in national house price inflation sees real (inflation-adjusted) house price inflation remaining in negative territory this year – for the fourth consecutive year. The one region where real house price inflation remains positive is the Western Cape, which is currently enjoying the seventh consecutive year of positive real house price inflation.

SOURCE: Pam Golding Residential Property Index & Statistics SA

For period January to September 2019

| PGP Index (average ytd) | Average HPI (nominal) | Average HPI (real) |

| National | 3.21 | -1.06 |

| Western Cape | 5.78 | +1.51 |

| Gauteng | 2.43 | -1.83 |

| KwaZulu-Natal | 3.15 | -1.11 |

SOURCE: Pam Golding Residential Property Index & Statistics SA

Regional trends

Notably, the Western Cape housing market has enjoyed real growth in house prices since late 2013, when it began diverging from the rest of the South African market, While the rest of the national housing market was experiencing a downturn, the Cape benefited from the influx of older, more affluent home owners as the semigration trend intensified.

However, from late-2017 until early-2019, the Western Cape housing market – though still outperforming the other major regional markets – experienced slowing house price inflation, bringing it back into line with the rest of the country.

While the recent revisions by Lightstone have removed an earlier rebound in national house price inflation, the Cape market appears to have reached a modest turning point, with house price inflation rising from a recent low of 4.97% in May 2019 to 5.12% in September (see below).

SOURCE: Pam Golding Residential Property Index

According to the PGP Index, price growth in Gauteng continues to lose momentum, while in KZN prices appear to have stabilised.

| PGP House Price Inflation (Jan-Sep 2019) | ||||

| average | < R1m | R1m – R2m | > R2m | |

| South Africa* | 3,21 | 5,40 | 2,55 | 0,79 |

| Gauteng | 2,43 | 4,79 | 1,66 | -1,05 |

| Western Cape | 5,78 | 12,60 | 5,10 | 0,00 |

| KwaZulu-Natal | 3,15 | 5,02 | 1,88 | -0,22 |

| SOURCE: Pam Golding Residential Property Index * SA national price band R2m – R3m, >R3m not represented |

||||

SOURCE: First National Bank

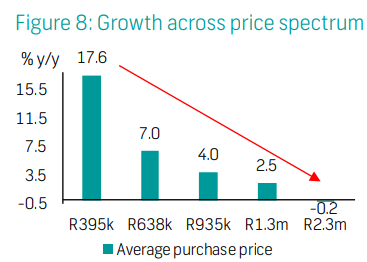

Lower price band is top performer

Breaking the lower price band down further, FNB shows that the sub-R400 000 price band is currently enjoying double digit growth, remaining the top performing nationally and across all major regions. According to the PGP Index, the Western Cape continues to show the strongest growth across all three price bands. The top price band is weakest in Gauteng while the lower price band is still registering double digit growth in the Western Cape, which suggests a high demand and shortage of stock.

SOURCE: Lightstone

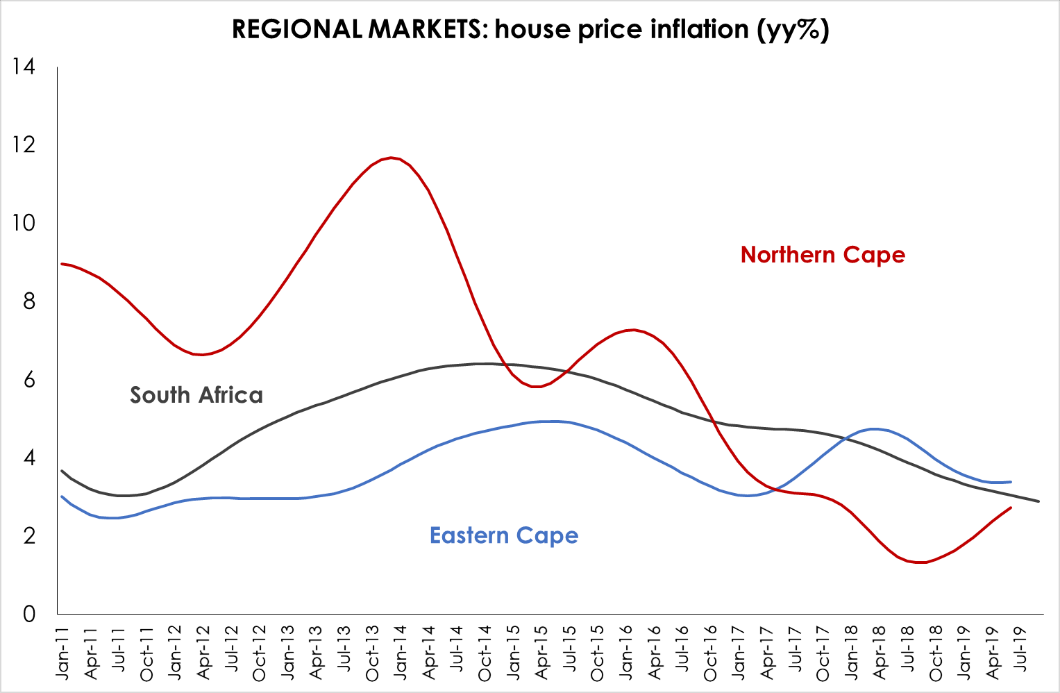

In the Eastern Cape, house price inflation also appears to be stabilising at a level of 3.37% after slowing over the past year, having averaged 3.43% during the first half of the year (latest available data). Eastern Cape house price inflation continues to outperform the national average by a small margin (0.24% average) during the first half of the year.

Positively, the Northern Cape is experiencing a rebound in prices, from a low of 1.32% in August 2018 to a high of 2.73% in June 2019 (latest data).

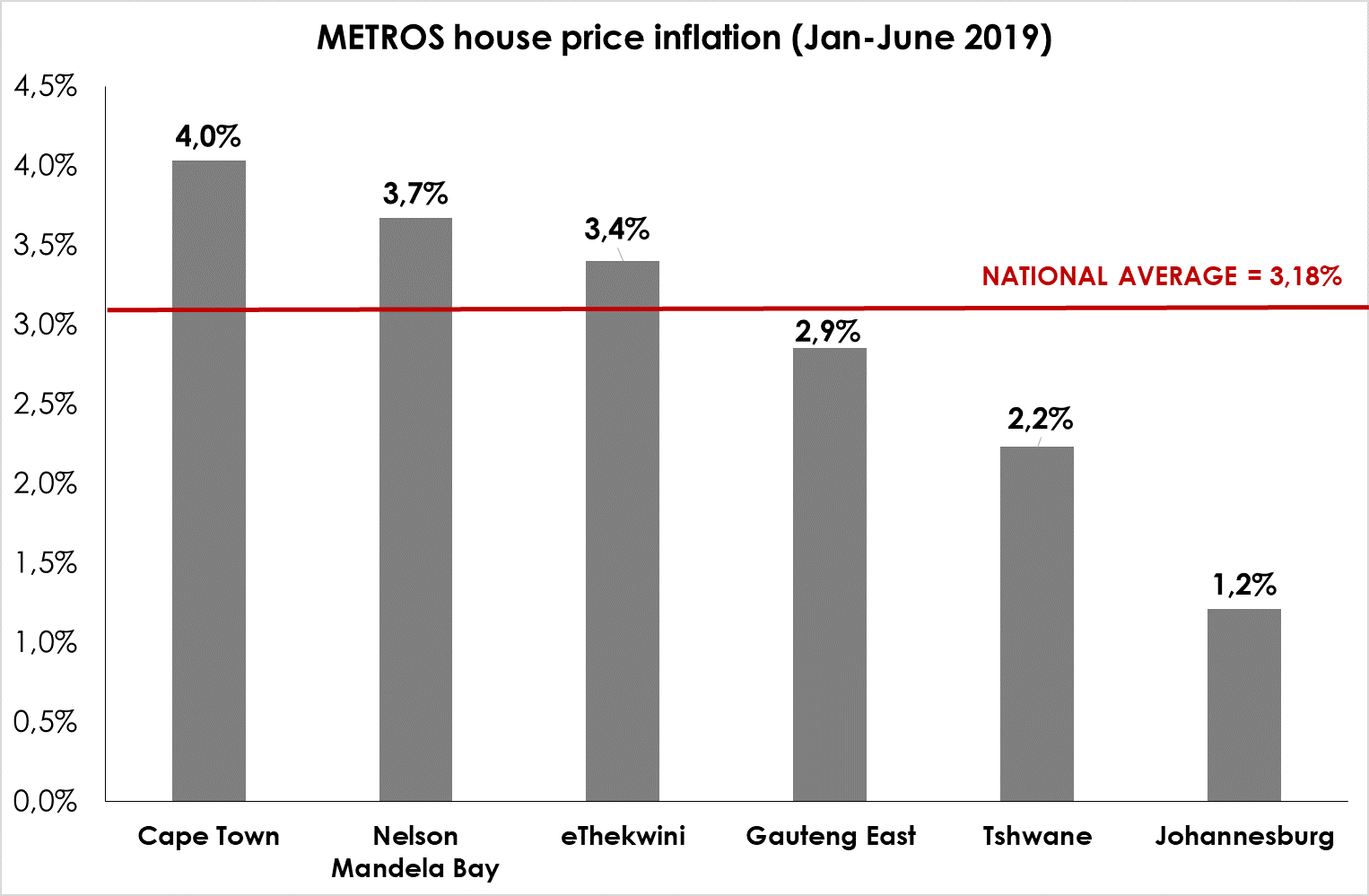

Metro housing markets

The three coastal metros continue to outperform the national market, with Cape Town remaining the top performing metro while Johannesburg (and Gauteng overall) remain the weakest.

SOURCE: Lightstone

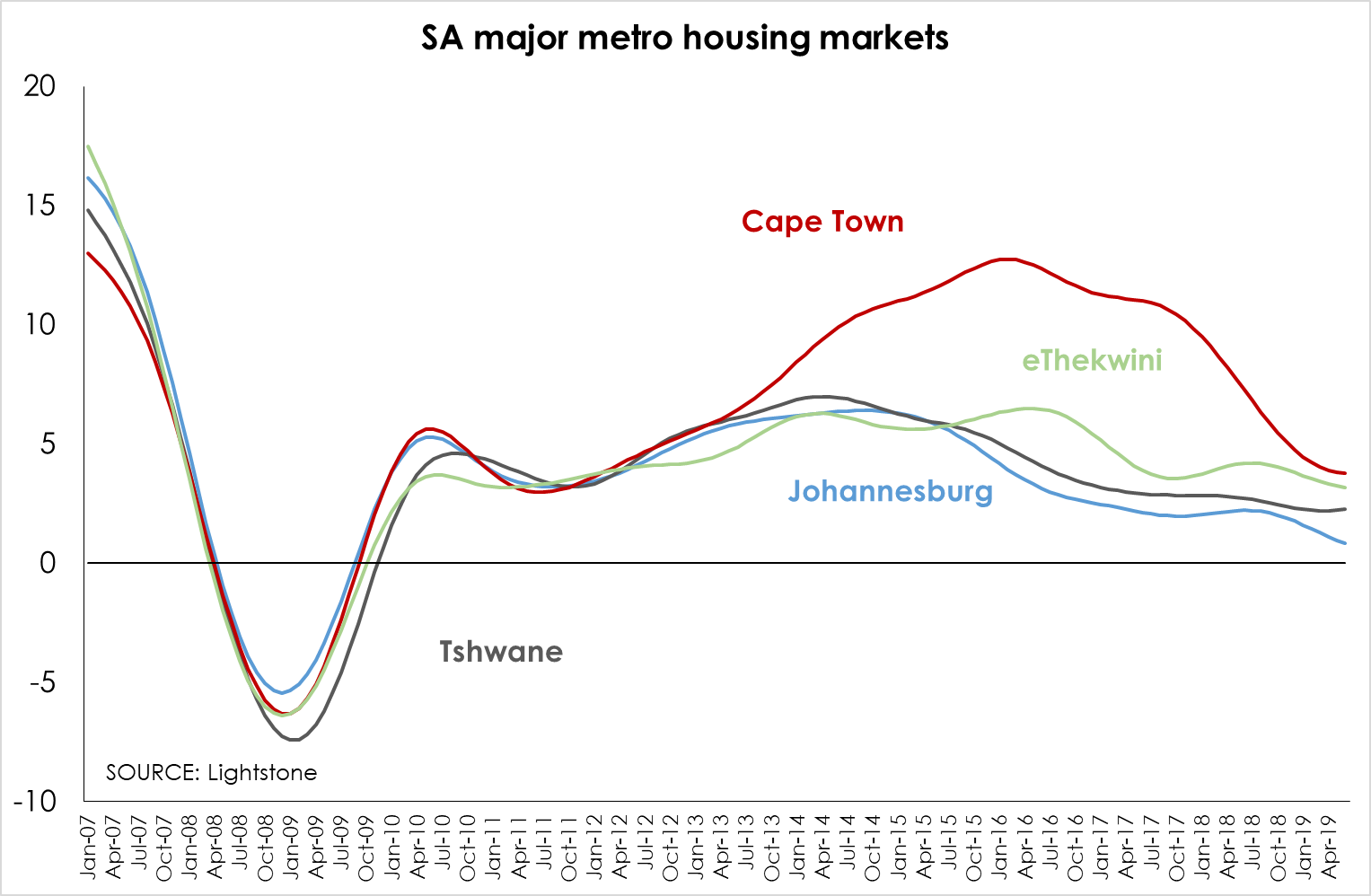

The rebound evident at a regional level (data to September 2019) is not yet visible at the metro level (June 2019 latest data). Nevertheless, house prices in both Cape Town and Tshwane metro markets are showing tentative signs of stabilising (see below).

SOURCE: Lightstone

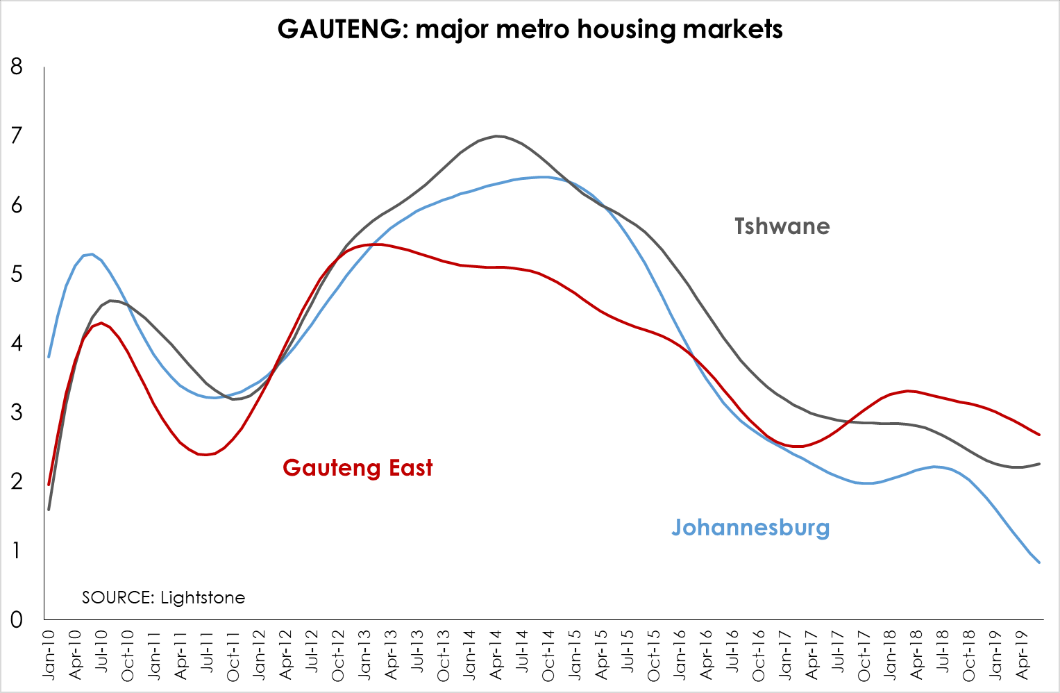

Metro housing markets in Gauteng, which is the weakest of the major regional markets, are showing diverse trends.

SOURCE: Lightstone

The slowdown in Johannesburg is rapid and is showing no sign of slowing or stabilising. Tshwane, as noted above, appears to be turning upward while Gauteng East is losing momentum but remains the top performing metro market in the region.

SOURCE: ooba

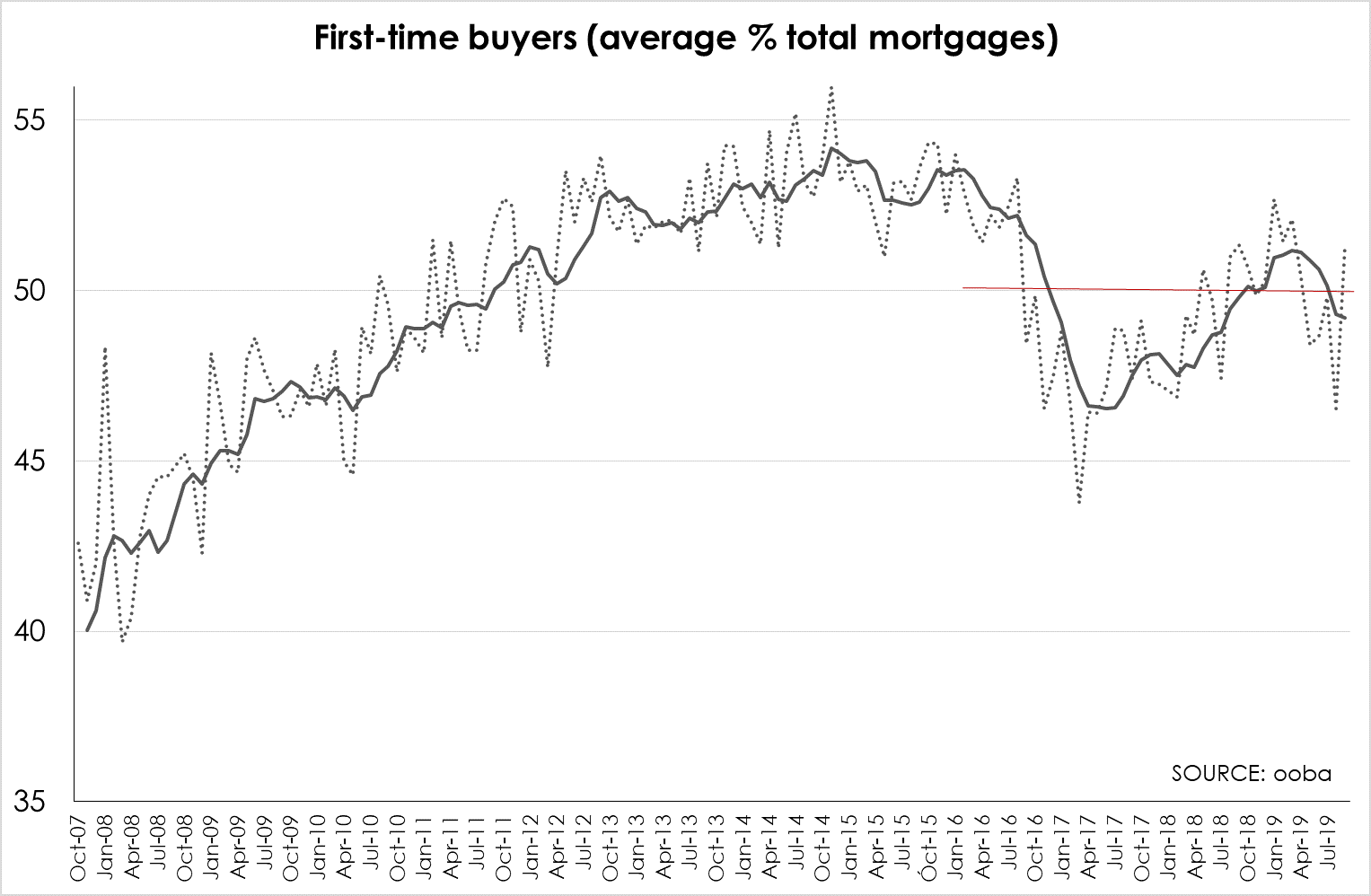

South Africa’s demographic profile means that young, first-time buyers provide a solid underpinning to the residential property market. So it is encouraging to see a marked rebound in the percentage of loans extended to first time buyers in September 2019 (51.4%). For the year to date (Sep’19) just over half (50.2%) of all loans extended by ooba have been to first-time buyers.

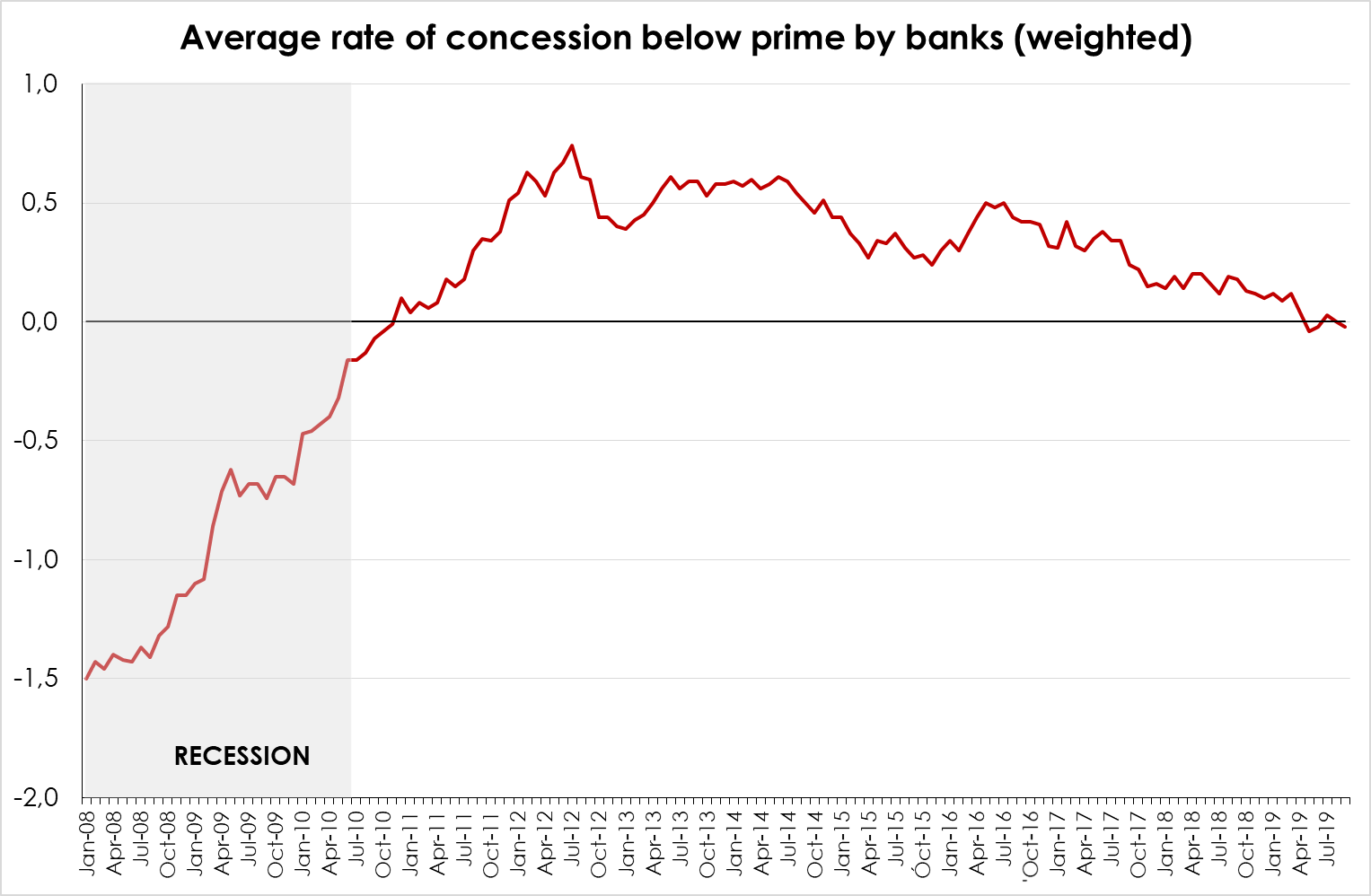

Further evidence of the appetite for home loans is visible in the improving loan conditions – with the average rate of concession falling below prime three times thus far this year. For the year to date, the average concession is just 0.04% above prime – the best rate charged since January 2011.

SOURCE: ooba

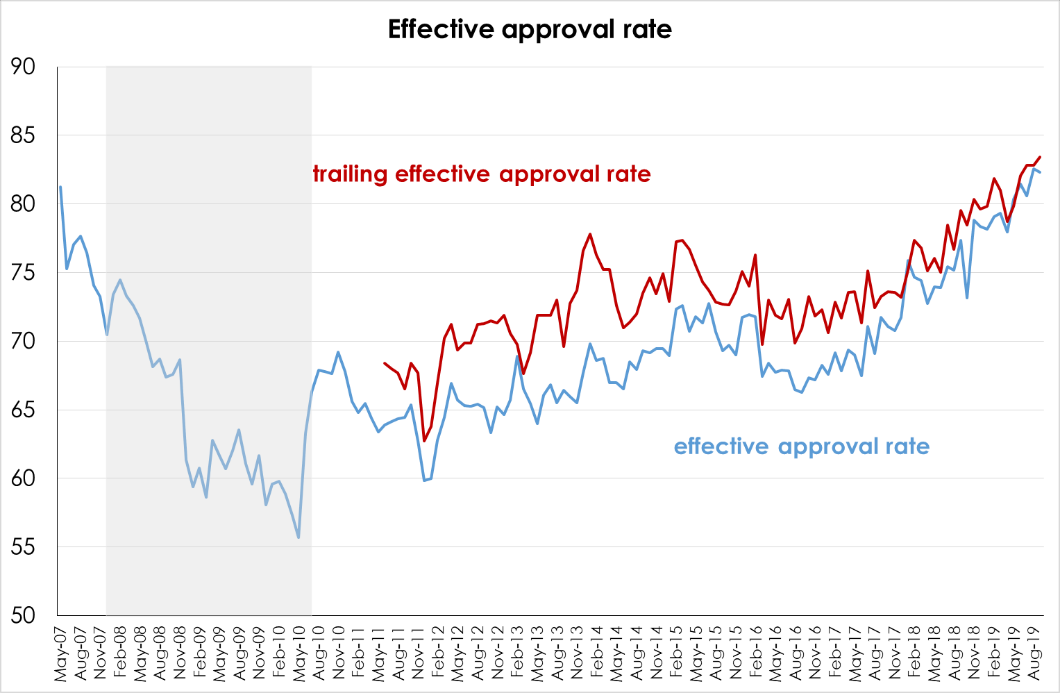

The effective bond approval rate continues to rise – reaching levels last seen just before the 2008/09 recession, rising to 83.4% in September and averaging 81.4% so far this year – up from 77.4% during 2018 overall.

SOURCE: ooba

The approval rate linked to pre-qualification rose to 89.6% in September and has averaged 88.6% during the year to date (Sept).

SOURCE: ooba

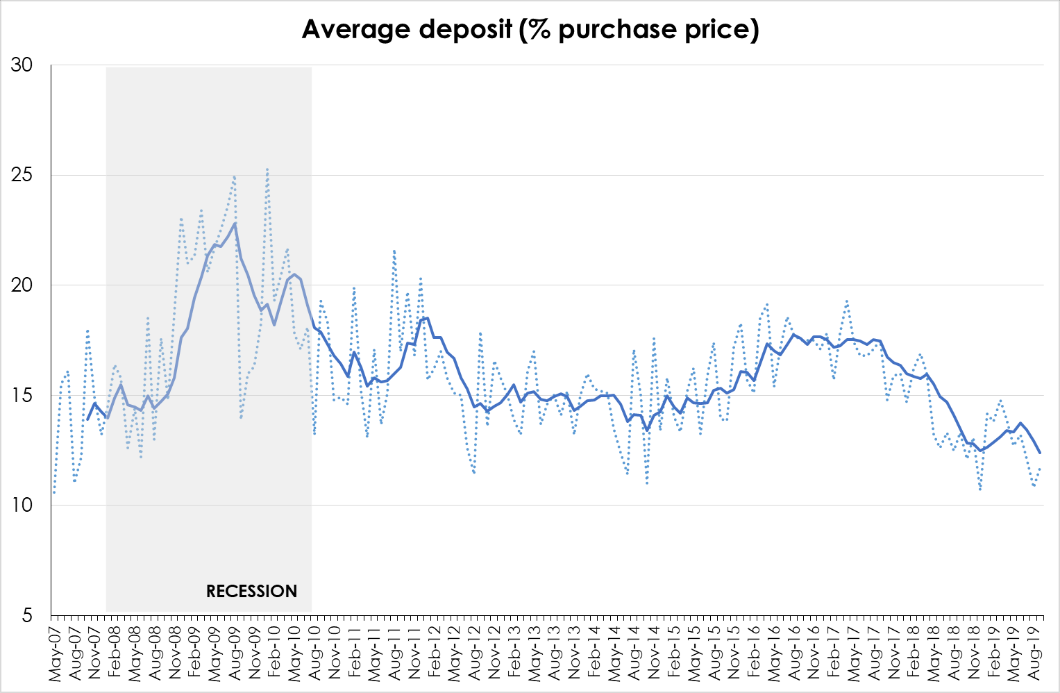

The average deposit is also declining, again reaching levels last seen just prior to the 2008/09 recession. In August the ratio of loans to value had declined to 10.8% before rebounding to 11.7% in September. For the year to date, the average deposit to loan was just 13.02% while for first-time buyers, the average deposit paid during the year to date is 9.38%.

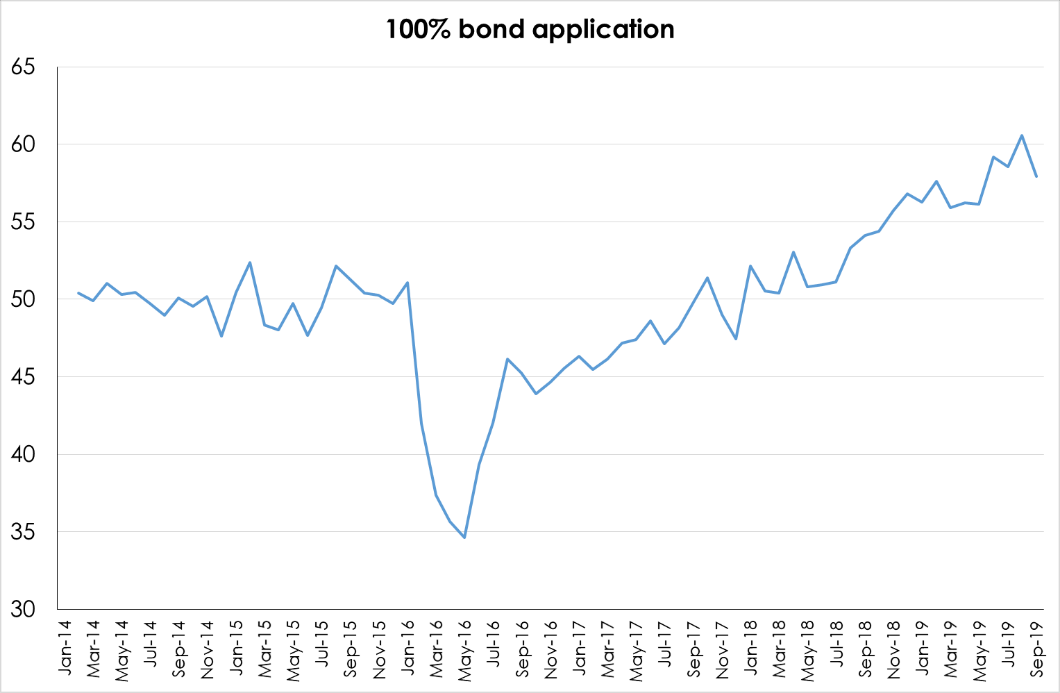

Applications for 100% bonds have risen steadily in recent years, reaching a level of 59% during the third quarter.

SOURCE: ooba

SOURCE: ooba

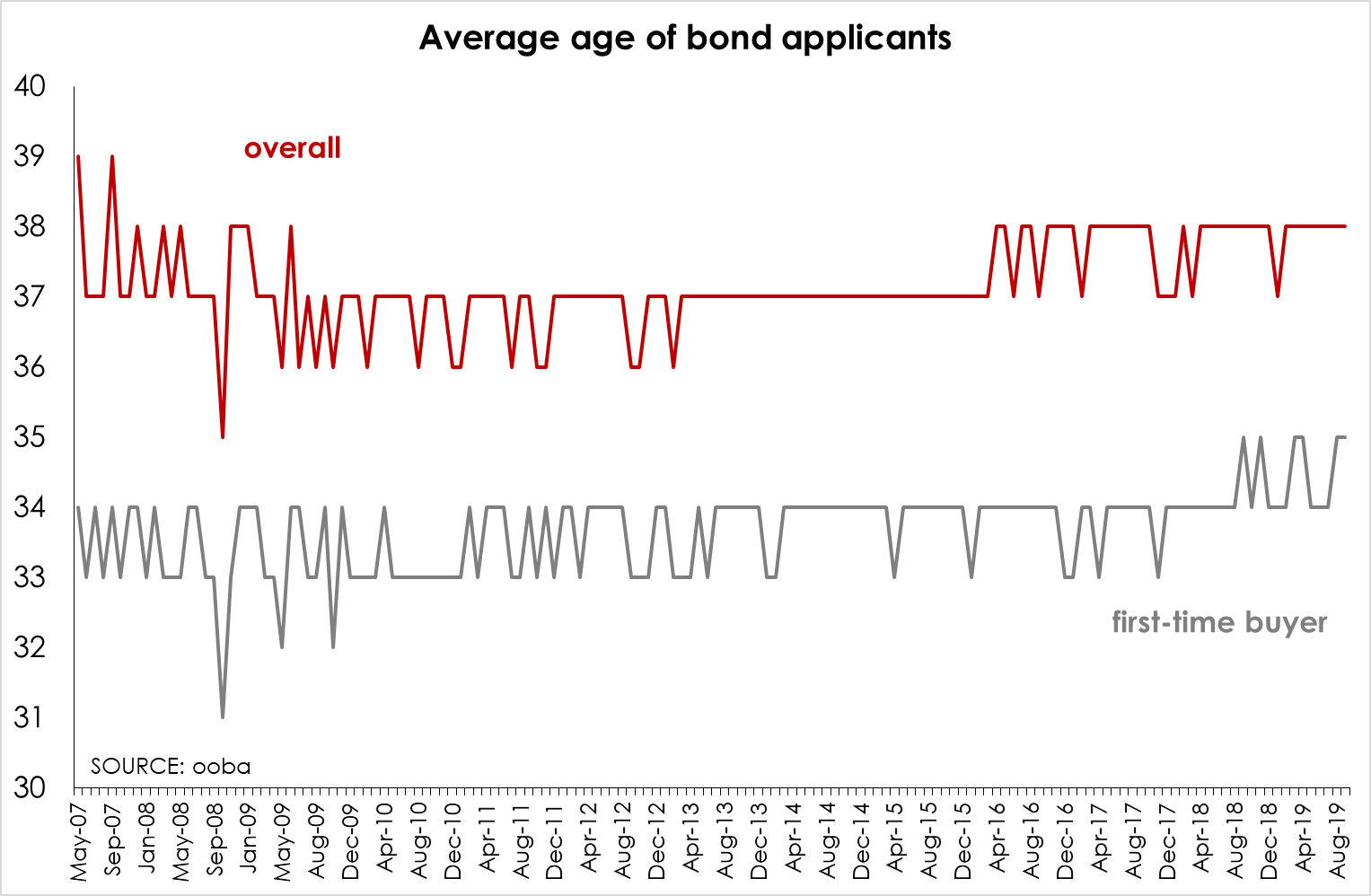

According to ooba, the average age of bond applicants overall has remained steady at 38 years for some time now, after rising from 37 to 38 in late 2016, while the average age of first-time buyers has risen in the past year from 33 to 34 years.

SOURCE: ooba

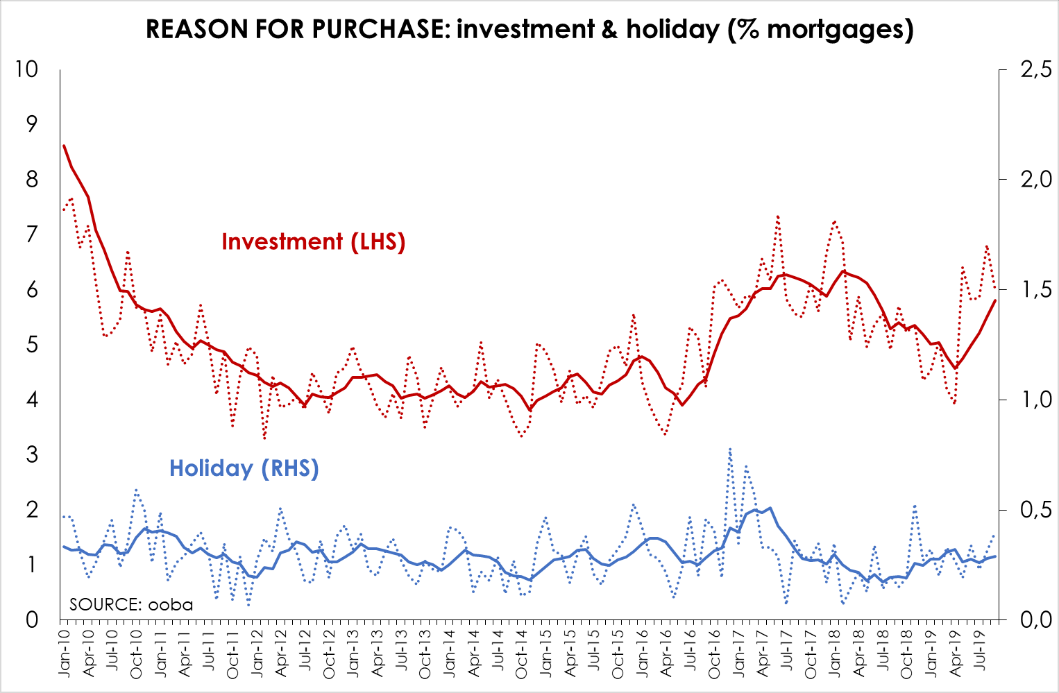

For the year to date, 94.3% of all mortgages extended have been for primary residences. While loans for holiday homes remains subdued at 0.3%, there has been an increase in demand for investment properties (buy-to-let) at 5.4% during the year to date.

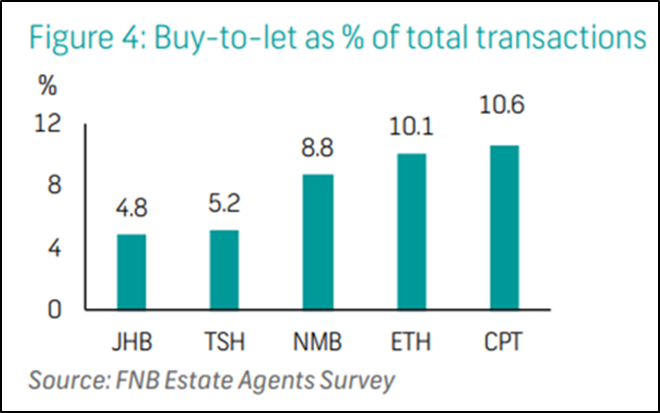

According to FNB, demand for investment properties has been particularly strong in the coastal metro markets – which are the best performing housing markets in SA, particularly Cape Town, with investment properties accounting for 10.6% of all properties sold during Q2 2019.

SOURCE: Lightstone

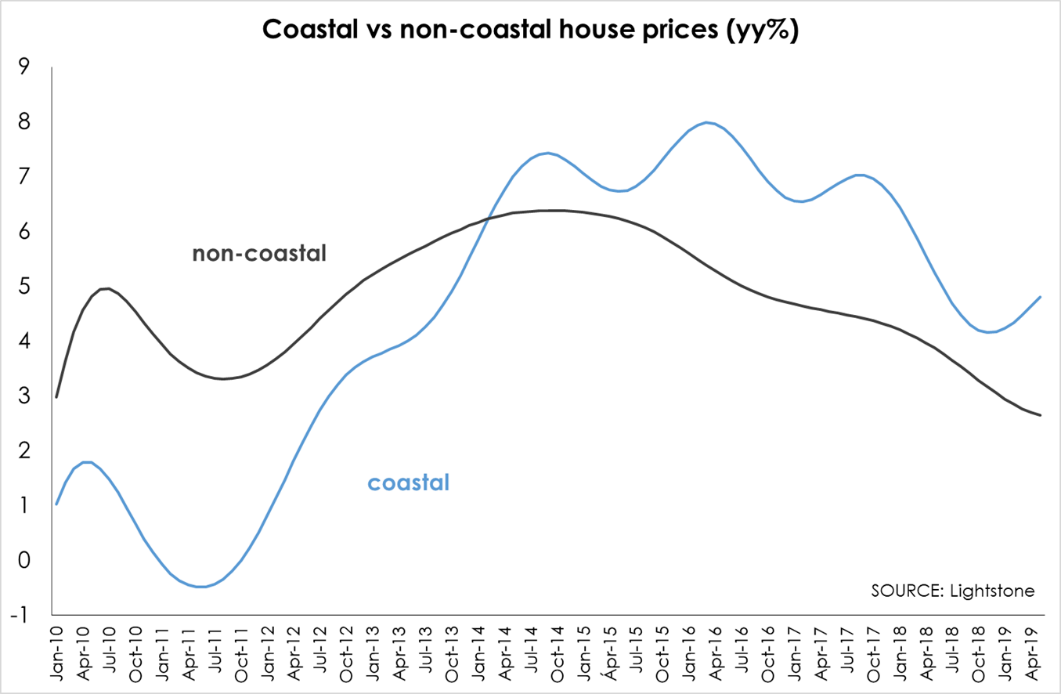

Coastal properties (homes located within 500 metres of the coastline) continue to enjoy a price premium which has risen from a low of 0.9% in Sep/Oct 2018 to a level of 2.13% in June 2019 (latest available data).

Sentiment a key driver of demand

It is not just about the ability of people to purchase a home but also their willingness (see chart below). One of the key measures of “willingness to buy” is consumer confidence, which is in turn driven by market sentiment as well as affordability. Nationally, consumer confidence rebounded slightly in the second quarter – with the ending of load shedding in the first quarter and the market-friendly outcome of the May general election contributing to the recovery. At current levels, consumer confidence is marginally above the long term average (and is not nearly as negative as business confidence, which is currently at a two-decade low).

SOURCE: Bureau of Economic Research

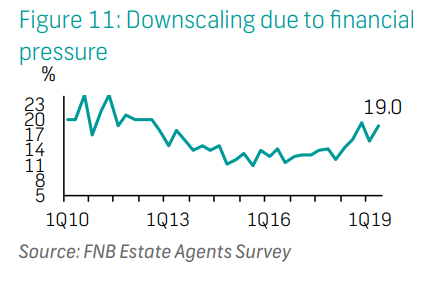

Downscaling remains a key theme – with 23% of all sellers offering that reason. It is also the dominant theme across all price bands. The second most popular reason for selling is financial pressure. While the percentage selling for financial reasons has risen to 19% in Q2 2019 this remains well below the levels seen in the wake of the 2008/09 recession (see chart below).

Emigration

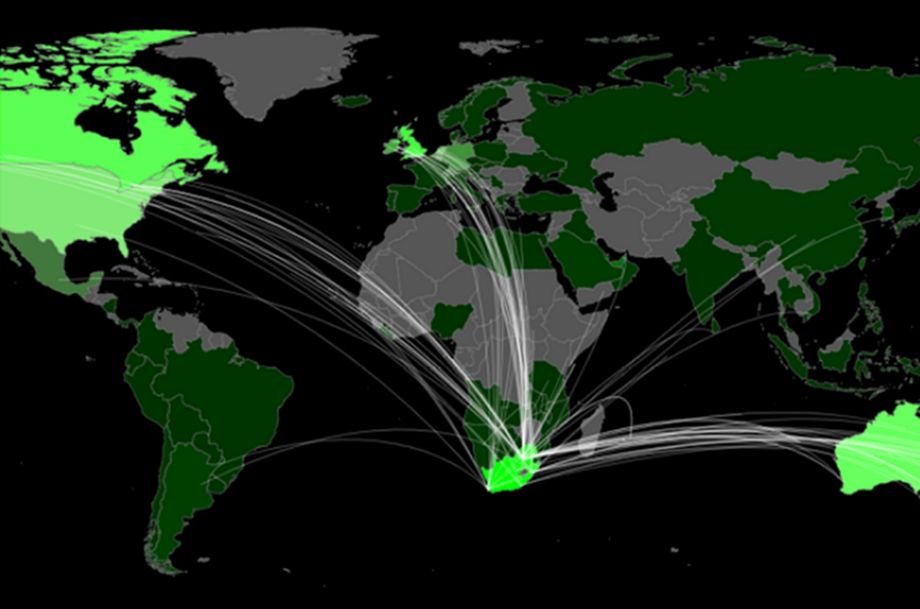

The same is true for emigration – which has become a more prominent factor over the past two years, according to FNB. Emigration sales have risen to 13.4% in Q2 2019 – which represents a 10-year high. While emigration sales are highest for the upper income groups, the increase in middle and lower price band sales due to emigration could reflect people selling their investment or holiday homes.

A map of where most South Africans are emigrating from (see below), shows that the majority of emigrants are leaving from Gauteng – a factor which is undoubtedly contributing to the subdued Gauteng housing market.

Market conditions: FNB Estate Agent Survey Q2 2019

The FNB Market Strength Index suggests the market is still moderately oversupplied, particularly in the middle- to upper-income areas. According to FNB It appears that the sectional title market is currently oversupplied, which is consistent with the surge in construction of new flats and townhouses, while demand and supply of freestanding properties is relatively evenly balanced.

Need for realistic pricing

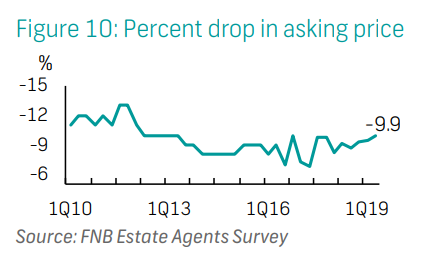

The fact that the market remains slightly oversupplied (imbalanced) is highlighted by the increase in the percentage of sellers who have to drop their asking price. According to FNB, this rose to 98% in Q2 2019 – the highest percentage of sellers since 2007. Furthermore, the average price drop rose to 9.9% in Q2 – slightly above the historical average of 9% since 2010 (see chart below). This underlines the critical importance of accurate, market-related pricing when a property is first brought to market. Buyers are well-informed and many under financial pressure, so a serious seller is advised to price right.

However, it seems that the supply of properties onto the market is responding to weak market conditions and is thus slowing – a positive for sellers.

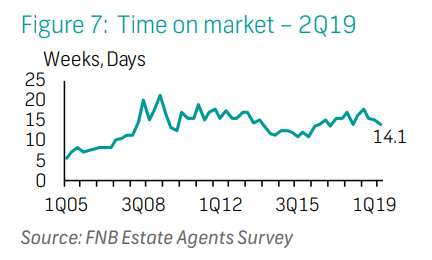

On another encouraging note, time on the market improved to 14 weeks and one day, down from a recent peak of 17 weeks and six days in Q3 2018, possibly due to the fact that improved affordability is attracting more buyers. According to FNB, current time on the market is approaching the long-term average of 13 weeks and four days.

SA rental market

Growth in national rentals has been slowing steadily since early-2017 – declining from 7.4% from year earlier levels in Q1 2017 to a low of 3.2% in Q3 2018. Growth in rentals has fallen below the prevailing inflation rate since Q1 2018 but has at least stabilised at 3.9% during the first half of 2019 even as the inflation rate continued to surprise on the downside. Real (inflation adjusted) rental growth declined by an average 0.5% during the first half of the year, according to PayProp.

SOURCE: PayProp Rental Index & StatsSA

While growth in national rentals has stabilised at 3.9% during the first half of the year, the performance of various regional markets has been more diverse.

| Regional rental Q2 | Rental growth Q1’19 | Rental growth Q2’19 | |

| Gauteng | R8 053 | +4.38% | +3.87% |

| Western Cape | R9 025 | +2.96% | +2.51% |

| KwaZulu-Natal | R8 171 | +4.62% | +5.43% |

| Eastern Cape | R5 840 | +3.18% | +3.52% |

| Average growth | +3.85% | +3.86% |

SOURCE: PayProp Rental Index & StatsSA

Rental growth in six of the nine provinces recorded stronger rental growth rates in the second quarter compared to the first. While the Western Cape remains the most expensive for renters, rental growth in the province continued to slow during the first half of the year.

In the Western Cape, we are finding that areas which remain popular include the Southern Suburbs, due to the schools in the area and proximity to Cape Town; City Bowl/Foreshore/Waterfront and Atlantic Seaboard in general for its appealing lifestyle and easy access to work; and the Northern Suburbs with its good schools, shopping centres, wine routes, medical and educational facilities and more affordable rentals, making it appealing for those working in the area or the Boland region, including Stellenbosch. Noordhoek has also become sought after, offering community living away from the hustle and bustle, as well as Woodstock/Salt River/Observatory as rentals are lower than the City Bowl and ideal for students and those commuting to the central city. We are also seeing an increase in demand for apartments to rent in secure developments, especially in the Southern Suburbs, City Bowl, Foreshore, Observatory and surrounding areas, where rentals vary from R7 800 for a bachelor unit and two bedrooms up to R20 000 plus.

Pam Golding Properties sales

Nationally, for the group’s financial year ended February 2019, the company achieved sales turnover of just under R18.8 billion despite the challenging economic and socio-political trading conditions experienced, and for financial year to date (seven months March to September 2019), we are currently on sales turnover of R11.6 billion, which compares favourably with R10.7 billion for the same period in 2018.

Reviewing our sales performance over the same seven-month period we are finding that sales volumes (units) are slightly up from 2018 levels. Notably, in terms of market share, we have increased our sales volumes by 29% in the price band from R12 million upwards – with sales above R25 million having doubled, and by 12% in the price band from R3 million to R6 million. In line with market trends, we continue to see high activity in the price band below R3 million.

Foreign buyers

During this period Pam Golding Properties sales to foreign buyers remain at more or less the same volume as last year, namely just over 3%. Emanating from some 36 countries around the globe, these buyers tend to purchase property across all price bands, but particularly between approximately R2 million and R6 million. Interestingly, we’ve seen a surge in buyers from Botswana, with UK and German buyers second and third in terms of volumes, followed by Zimbabwe, Switzerland, the Netherlands, France, Denmark, USA, United Arab Emirates, Namibia, Mozambique, Congo, Zanzibar, Turkey, Tanzania, Sweden, Spain, Russia and even Romania, among others.

Market overview

While the last real boom was just over a decade ago (2003-05) the residential property market in South Africa has demonstrated ongoing resilience in recent years despite the challenges of a muted economy, socio-political impacts and drought. The market is, however, nuanced and varies from region to region and across metros and towns, with pockets of excellence in high demand areas and nodes around the country, coupled with a strong demand, as stated, in the price band below R3 million. What we are seeing is that only correctly priced properties are selling – often in weeks or days, sometimes even hours of listing.

Currently, sound investment opportunities for the savvy buyer and investor are still available in the various sectors of the market which continue to thrive. We also have a sense that there is the possibility that the economy has the potential to improve, and that from a cyclical point of view the property market is at or near the bottom of a down cycle, and hence this is potentially a good time to buy. Property markets through the ages have behaved in cyclical patterns and there is nothing to suggest that the current environment is systemic or permanent. As with all property investment decisions, due care needs to be taken with location, price and resale potential, regardless of the particular market cycle.

As per usual, the property market is not a case of one-size fits all, with sales activity in different regions and with higher demand and activity in sought after centres and conveniently located nodes around the country. These include Cape Town central, Stellenbosch and Somerset West in the Cape Winelands, Pretoria and Rosebank in Gauteng and the KZN North Coast (uMhlanga, Ballito and Sibaya). Well-located growth nodes, which have mixed-use developments, continue to see elevated levels of activity as these meet the abovementioned demand, offering a secure, live-work-play lifestyle appealing to a growing number of South Africans across a wide range of income bands and age categories.

Further areas of growth include relatively more affordable homes in towns traditionally considered retirement or holiday destinations, particularly those experiencing strong growth in amenities (medical and education) which reduce the necessity to travel to a large neighbouring town or city. A good example of this is Knysna on the Garden Route, also Jeffreys Bay and to some extent St Francis Bay on the Eastern Cape coastline.

Current and ongoing trends in the market:

Sectional title: There is an ongoing demand for sectional title homes, more compact homes with lower maintenance and lower operating costs, and homes in convenient locations close to schools, the workplace and all amenities – thereby allowing homeowners and tenants to avoid heavy traffic congestion. This is particularly evident in key hubs or growth nodes such as Menlyn Maine in Pretoria, Sandton, Cape Town central and uMhlanga. More single people are buying property, which is also driving demand for sectional title living, which is not surprising as in today’s world many people are delaying marriage or not marrying at all. We’ve seen large numbers of millennials (aged 22-37) buy homes in recent years. Aside from having appeal for the younger generation, sectional title buyers include professionals who travel frequently, downscalers and retirees who travel overseas to visit family.

Semigration: The semigration trend will continue to the coast, primarily the Garden Route and KZN – Durban and north to Ballito, and the Western Cape – including the Boland and Overberg. Areas such as Ballito and Knysna, also St Francis Bay, Port Alfred and Jeffreys Bay, which were previously considered holiday hamlets, have become primary residential areas. In addition to attracting semigrators, Knysna is currently seeing an influx of buyers from Europe. In George, currently over half our home buyers are from regions outside the Garden Route – mainly from Gauteng and the Western Cape, followed by Mpumalanga and the Eastern Cape. Interestingly, outside of estates, George is seeing a considerable reduction of 20.8% in available stock when compared to the same time last year (August 2019/18). On the KZN North Coast, we’ve recently seen as much as 60% of our buyers for new off-plan developments originating from Johannesburg, while Sibaya near eMdloti is also in demand due to its close proximity to King Shaka International Airport.

Value-for-money and hotspots: Country towns inland offer exceptional value especially for retirees, and from a coastal perspective, we may see increased interest in KZN areas from Amanzimtoti through to Port Shepstone on the South Coast, where lifestyle, cost of living and house prices are affordable. In the meantime, the KZN North Coast is seeing developments still selling well and correctly priced stock moving. An influx of Johannesburg commuters and semigrants moving to the coast has kept the developments market alive. In addition, KZN is still well-priced compared with the Western Cape and affordable to the local market. Sibaya is this region’s most buoyant new precinct, having enjoyed exceptional sales over the past two years and achieving record prices on vacant land at Signature Estate, where luxury homes range from R20 million up to R50 million. However, at Saxony at Sibaya, a luxury development with sea views, apartments and penthouses are selling starting from R1.85 million.

We are expecting our new development, Sibaya Sands, to be well received by the market as it caters to both an investor clientele as well as an end-user market, with prices starting from under R2 million. uMhlanga sectional title is also sought after and the beachfront node popular as there is limited supply in this prime area. Stable Durban North continues to hold its own as a primary residential market that is well-priced and offers a family lifestyle with an abundance of schools. In uMhlanga, Somerset Park and Sunningdale are becoming more and more popular as you can buy small three-bedroom, family homes in these nodes for under R3 million, while apartments trade for around R2 million. In Durban, the Florida Road area is a hotspot with a one-and-a-half bedroom flat with parking selling in three days for R980 000, close to asking price.

Krugersdorp on the West Rand, with its new developments, are a good buy and should provide excellent returns in five years. Due to its good value-for-money offering, people are buying here and are willing to commute to Johannesburg and Pretoria. In the new Copperhill Lifestyle Estate development you can buy a three-bedroom, 2.5 bathroom sectional title home of 165sqm with single garage and carport and sizeable private garden for R1.7 million. Catering for the younger, middle-class buyer, sectional title developments are on the increase and range from R1.65 million to R2 million. Three new developments are being launched in the future in the Homes Haven area.

In Gauteng East, ‘The Neighbourhood’ is likely to become ‘the’ estate in this region. Providing a clear indication of investor confidence in the area, this new development is in the historic Linksfield suburb, with 315 stands priced from R2 million to R4.2 million. Phase One sold out in days, underlining the demand that exists for prestigious living within a secure environment, close to important amenities. This development also features a sectional title component called The Lofts and a shopping centre, The Square. In addition, catering for the growing demand for homes in Gauteng East, large tracts of open land between Benoni, Boksburg, Kempton Park, Edenvale and Greenstone have been developed with clusters, townhouses and shopping centres. Here you can acquire a quality two-bedroom, two-bathroom sectional title unit for R850 000, ideal for first-time buyers, as well as a top-end two-bedroom, two-bathroom unit for just R2.6 million in upmarket Infinite development in Bedfordview.

The greater Fourways area – in suburbs such as North Riding – has also seen many new developments coming onto the market particularly in the under R1 million bracket, while continued commercial development in Rosebank and Sandton has seen the construction of some large sectional title developments. People look to live in a radius of offices and good schools so The Parks, Westcliff, Saxonwold, Parkhurst, Morningside, Atholl, Illovo and Inanda continue to attract people for correctly-priced properties. This trend is further driven by offices such as Discovery and Sasol in Sandton which house some 8 000 workers who in some cases look for convenient living and lifestyles. Access to Pretoria and the burgeoning residential growth on the N14 which has been upgraded will enable access into Fourways, the new areas around Steyn City and the Centurion area of Thatchfield.

The entire Waterfall area situated in Midrand has seen increasing growth over the last year, attracting both investors as well as buyers seeking a long-term lifestyle. Large companies such as PricewaterhouseCoopers and Deloittes moving their head offices to the area and the presence of good schools are fuelling the demand for residential accommodation. The Waterfall area also provides upmarket lifestyle apartment living including all amenities such as gyms, restaurants, movie centres, as well as an amazing pool and recreation facilities. In Waterfall Estate we recently sold a R4.9 million two-bedroom home in three days and a R5.5 million two-bedroom home in two weeks.

In Pretoria in Tshwane Municipality sales continue apace in the Trilogy Collection, a R1.16 billion residential development in the major mixed-use Menlyn Maine precinct. With a total of 531 apartments when completed, 374 units in Phase 1 have been sold with limited units available in Phase 2 comprising 157 apartments. Such is the demand that apartment prices have risen by as much as 20% since the development was launched in 2016, underlining the demand for a live, work, play lifestyle in this urban setting. In Phase 2, prices range from R1.6 million for studio apartments, R2.2 million for one-bedroom units and R4.8 million for two-bedrooms. Part of Phase 2 comprised the sold-out Platinum Collection, exclusive apartments on the 10th and 11th floors, plus a double-storey, 574sqm presidential suite on the 12th floor which sold for R20.5 million.

In the Western Cape, value is driving sales in Cape Town’s Southern Suburbs across all price bands and we expect this to continue. Top end sales include a modern, double-storey Bishopscourt home which fetched R41.3 million. We also recently concluded the highest residential sales transaction in the Southern Peninsula for a five-bedroom house in the exclusive lifestyle and security estate, De Goede Hoop, for R29.5 million. In Bergvliet/Meadowridge we find older homes to be renovated are always popular, but at the right price, and in Rosebank, we recently sold a three-bedroom home in just five days at a fraction below the asking price of R3 million. On the Western Seaboard, the areas of Tygerhof and Sandrift, nestled between Century City and Milnerton and with its proximity to major arterial routes, are definitely beginning to upgrade. Currently the entry level is around R1.8 million. Opportunities are still evident in the under R2.5 million market, in areas such as Sunningdale, Parklands and some of the older areas of Table View, as well as generally in the sectional title market. With its affordability at entry level, proximity to the city and beach, magnificent Table Mountain views, watersports and laidback lifestyle, the Western Seaboard is an appealing place to live.

The Atlantic Seaboard offers a compelling lifestyle proposition, so it remains a perennial hotspot, drawing local, national and global buyers and investors, attracted not only by the investment opportunity but also its highly appealing and convenient, luxury lifestyle, with developments such as the V&A’s Waterfront Marina, Harbour Bridge and Canal Quays on the adjacent Foreshore doing well. Top end sales on the Atlantic Seaboard are currently frequently in the R20 million to R40 million plus price range.

In the Boland region, the Northern Suburbs has seen huge commercial development, including new road infrastructure, businesses and restaurants, and in particular Durbanville’s commercial hub with the opening of Durbanville Square. Curro is also planning its first university on the outskirts of Durbanville in 2021 and, from our experience in student towns like Stellenbosch, we anticipate a meaningful positive impact on prices in the area. This may not be the size of Stellenbosch, but it will create opportunities for investors, student accommodation and a demand from lecturers to live in nearby suburbs such as Graanendal, Vierlanden, Pinehurst, Uitzicht and Langeberg Ridge. And due to the growth around Tygervalley, with the business and financial sector moving offices to the area, we are seeing a demand for property for Airbnb and guesthouse accommodation in nearby areas such as Rosendal, Ridgeworth, Kenridge, Bella Rosa and Tygervalley Waterfront.

In the Helderberg area, buyers have over 25 developments to choose from and, with competition in the resale market, the area offers value for money compared to many other towns in the Western Cape. Demonstrating sound return on investment, in Andringa Walk in Stellenbosch, a two-bedroom apartment registered in 2015 for R2.65 million and a two-bedroom unit in this development sold through Pam Golding Properties in October 2019 for R4.3 million. The new road being constructed connecting Technopark and Polkadraai will make Longlands Country Estate and Bosman’s Club – a new development comprising 46 units starting at R1.4 million, a very savvy investment now before the road is built. As mentioned under student accommodation below, we are also marketing units in The Niche, a new apartment block in Paul Kruger Street, so with another five blocks in the process of rezoning, this will turn the entire area into a student hub in the next few years. With the escalation of building cost and high demand for student housing, being one of the first to buy will be a very strategic investment decision.

Along the Whale Coast, buying opportunities include affordably priced vacant land starting at R275 000 for 600sqm in Bettys Bay, and seafront properties in this coastal hamlet from R1.95 million for a 1 520sqm seafront stand to R3.995 million for a four-bedroom front row home in Rooi Els.

Other hotspots which present good value can be found anywhere in metro hubs across the country in townhouse or cluster communities with a price tag of R1.5 million and where there are pools, a clubhouse or other facilities. Also good, older areas around sought after government schools which are situated in areas where there is little through traffic might become in demand and increase their security levels.

Estate living: This remains sought after, especially eco-estates and those which provide a range of amenities, even schools and leisure activities. Then there are what one could refer to as mixed-use estates, such as the new estates being developed on the periphery of Somerset West, a town experiencing a virtuous cycle in that the surge in residential development has sparked commercial growth to cater for the growing population. Shopping centres and offices are being developed to service the newer, outlying areas of town while new residential developments along the N2 also include commercial and industrial components. For example, Paardevlei, on the old AECI grounds, is a self-sustaining town with residential, commercial and light industrial areas.

There is also a strong focus in estates on creating a greater mix of price bands and retirement developments, ensuring broader appeal both in terms of available homes and amenities, such as shops, educational and medical amenities.

With land in Stellenbosch a scarce commodity, welcome new developments include Welgegund Domaine Prive, a new 32 erven boutique estate in Paradyskloof, close to the new Mediclinic and the very popular Brandwacht Aan Rivier, where we are selling erven from R2.1 million to R5.7 million for stands from 260-600sqm. Estates located in Paarl are also very popular because of the security and country lifestyle offered, while Wellington offers a more affordable country lifestyle, such as Stadsig Private Country Estate – considered the best location in town. In Pearl Valley at Val de Vie Estate in Paarl, we recently sold a home for R33 million – the highest price achieved to date in Pearl Valley and Val de Vie.

In Olivewood Private Estate at Cintsa in East London a boutique hotel has just been launched in addition to an offering of a number of value-added facilities on site to pique the interest of prospective buyers while, a new development at Toboshane in Dorchester Heights, conveniently accessible to the city (East London), will see 208 erven coming online in the next three years.

On the outskirts of Ballito area on the KZN North Coast, Pam Golding Properties is marketing vacant land in the 411ha Seaton Estate, a new-generation, luxury estate with the emphasis on sustainable living and a unique, organic way of life. Residents are able to reconnect with nature and even pick their own fruit and vegetables from the estate’s private farms and yet are located only 15 minutes to King Shaka International Airport. In the Ballito market there is huge growth with several other new developments on offer along the coast in Sheffield, Zululami and Elaleni – all top-quality estate offerings at great value-for-money pricing.

Estate living is on the increase in Port Alfred, notably the Royal Alfred marina, Misty Waves private Estate and the new development, The Reeds, where prices range from R1.4 million to R17 million. Pam Golding Properties recently sold a six-bedroom property in the Marina for R8.5 million – the second highest price ever achieved on the estate. Knysna on the Garden Route retains its high appeal with a number of highly sought-after estates such as Simola and Pezula.

Lightstone estimates that there are just over 450 000 properties located within approximately 8 600 estates across South Africa, 80.9% of which are freehold. There are also an estimated 214 retirement developments located in estates. While total estate sales have slowed in recent years in line with the overall slowdown in the national housing market, estates have retained market share, accounting for around 14.5% of total market sales, with buyers generally prepared to pay a premium to enjoy the lifestyle. In 2010 Gauteng accounted for about 55% of all estate sales, a figure which declined to under 45% by late-2016 and early 2017, but this has since risen once more, although it remains below 50% of all sales. In the Western Cape estate sales rose from just over 20% of national sales to over 30% in late-2016/early 2017 before drifting lower, and averaging at 27% during the year to date. KZN estate sales rose from around 5% of national estate sales to about 6.5% before declining back to around 5%.

Repurposing of old buildings: With an ongoing shortage of student accommodation around the country, we anticipate seeing an increasing trend towards old commercial buildings being redeveloped and repurposed to cater for this growing demand. This is already occurring in major centres. The repurposing of old buildings for mixed-use developments is seen in Cape Town’s Southern Suburbs, while parts of Johannesburg are seeing old light industrial spaces being converted into affordable housing close to transport hubs. In Fox Street in Johannesburg’s eastern CBD, a major rejuvenation project, Jewel City, comprises six city blocks, which are being redeveloped into office and retail space along with residential accommodation. Other amenities – including a school, gym and clinic – will also ultimately form part of the development.

Sustainable homes: The sudden recurrence of load-shedding, coupled with rapidly escalating costs of electricity and water shortages, has seen homeowners and tenants increasingly turning towards homes with ‘green’ features. This is a trend which we anticipate will continue to gather momentum and become more widespread across all areas and price bands. Pam Golding Properties recently sold a luxury home in Glencairn, made from seven shipping containers welded together to create an elevated, double-volume structure with 180-degree views of the sea and mountain for R4.85 million.

Student accommodation: The shortage of accommodation for students near universities and colleges continues unabated – a trend we believe will continue and strengthen in 2020. During the past year Pam Golding Properties sold close to R1 billion in student apartment blocks. Last year the student apartments in Stellenbosch were 99% fully let for the entire year. One of the new student developments in Stellenbosch that presents an appealing investment opportunity is The Niche, a 51-unit development with bachelor, one, two and three-bedroom units from R1.5 million and ideally suited to student needs. Also catering for this demand in this university town is Beau Vie on Stellenbosch University’s Green Route (which offers additional security for students), with bachelor units priced at R1.995 million and one-bedroom units from R2.37million. Properties on this route are highly sought after and can command prices of around R66 000 per square metre.

With ongoing demand for student accommodation in Pretoria, we are seeing more tertiary students looking for private housing with good security and located close to places of learning. There’s been a steady increase in investor interest in the student market, because of the rental returns of between 13% and 15%. One such development is iQ Brooklyn, the new upmarket student accommodation with apartments priced below R1 million and presents an attractive investment opportunity for buy-let-investors. iQ Brooklyn provides an array of amenities including Wi-Fi, central DSTV services, pre-paid electricity metering, swimming pool and sun deck, lounge and cafeteria facilities, laundry services, 24-hour security with biometric access as well as study and assignment rooms for groups.

Apart from the major centres, demand for student accommodation extends to other areas such as Port Alfred, home to Stenden University and the 43 Airschool, which contribute towards the demand for sectional title properties as student accommodation or property investment with a strong rental return. Current sectional title units in Port Alfred sell between R500 000 and R4 million, while Summerstrand in Port Elizabeth enjoys a strong demand for student accommodation, with apartments going for R450 000 for one or two bedrooms to over R2 million for a front row block with sea views.

Increasing demand for offshore property

According to our International Division, Pam Golding International, increased demand for international property is being fuelled by a desire to diversify investment portfolios with a rand hedge. The need to diversify, coupled with demand for offshore citizenship, has seen increased uptake by buyers investing in residential property in Portugal via the Golden Visa Programme as well as a surge in interest in the US EB-5 Programme for access to a Green Card and the Grenada Citizenship-by-investment programme. Notwithstanding this, property in Mauritius and the UK remain firm favourites with SA investors.

It’s not surprising that Lisbon features strongly on the radar of such investors, as according to the Emerging Trends in Europe 2019 report, it is currently the top-rated city in Europe for overall investment and development prospects in 2019, having leapfrogged 10 places to number one.

In Portugal buyers invest mainly for EU Residency, while in Mauritius – which has retained its pole position as 1st on the African continent in The World Bank ‘Doing Business 2020 report, it’s a combination of residency and leisure or second home acquisitions. In the UK it is purely for investment in hard currency, a hedge against political instability and diversification. In Portugal, the €350 000 Golden Visa developments in Lisbon, Porto and Cascais remain the most popular.

Since May 2019, Mauritius has experienced a noticeable ramp-up in property purchases that offer South Africans permanent residency, as well as those buying for pure investment. The Mauritian economy and currency continue to perform very well in the global arena with a buoyant real estate market driven by those relocating for work opportunities as well as holiday and retirement.

Mauritius remains an attractive destination for South Africans due to proximity and the easy ability for expats to oversee their business interests and investments in SA. Mont Choisy Le Parc Golf and Beach Estate continue to attract attention from high net worth individuals looking for an exclusive lifestyle in Grand Baie, with Phase 1 and 2 completed and numerous resales concluded. Phase 3 – called Mont Choisy La Reserve – has just been launched with 30 apartments and 25 villas. Ki Resort Apartments with Phase 1 comprising 70 units in Grand Baie close to sold out has attracted buyers looking for a pure investment purchase as well as those looking to spend US$500 000 to gain permanent residency plus access to the developer’s private beach club facility.

On Eden Island in the Seychelles, over 500 or 95% of homes are already completed and 550 sold in this vibrant, cosmopolitan community. Underscoring the investment returns is the fact that 25% of homeowners own more than one home on Eden Island. Prices of units currently start at US$455 000 and all owners qualify to apply for Seychelles Residency.

On the African continent, a standout country is Kenya, which is experiencing a generally positive outlook for its economy and housing market, particularly rentals, and with a large number of investment type buyers. Key growth hubs are mostly in Kiambu and Movoko due to affordability and also growth in infrastructure, mostly roads, schools and hospitals that are making these nodes more accessible and desirable. An interesting project marketed by Pam Golding Properties Kenya is Garden City, developed by Actis, a well-known private equity fund. This is a mixed-use development with a fully fledge mall, plus 159 two- and three-bedroom apartments and 56 semi-detached four-bedroom townhouses, residents’ gym, pool, clubhouse and children’s play area. Prices of the residential units are KSHS 17million for two bedrooms, KSHS 24 million for three-bedroom apartments and KSHS 35 million for the townhouses.

In Mozambique, we are currently marketing three- and four-bedroom beach villas in the exclusive San Martinho Beach Club Resort in Bilene in the north of Maputo, with a protected natural lagoon surrounded by pearly white sandy beaches and set on 43ha of lush, tropical gardens and 1.3km of pristine private beaches. Prices are from MZN 16 million. This kind of project appeals to locals and international buyers including South Africans who want to own a property and experience regular holidays in Mozambique. For an additional about MZN 1.8 million for furniture, properties can be included in the rental pool.

In Zambia, where residential property development is a relatively new concept, an increase in road infrastructure in Lusaka and the Copperbelt has seen a number of emerging residential areas becoming sought after areas for home owners. Other key hubs are Roma, Kabulong and Ibex Hill, which are well established residential areas in close proximity to amenities such as schools and shopping centres. The main residential trends in Zambia are for cluster developments, very similar to those we see here in South Africa. Currently we are involved in leasing out office space in the new Standard Chartered Head Office development an 8 000sqm office block, of which they will occupy 6 000sqm. Office space from 250-1 000sqm is let at US$30 per square metre. Key is its prime location in the financial hub of Lusaka with Citibank, Liquid Telcom and Barclays Bank nearby.

Outlook: cautiously optimistic

A key positive for South Africa’s housing market is the country’s young population – which ensures a steady increase in potential new homeowners entering the housing market each year, providing a solid underpinning for ongoing demand for homes. The impact of these first-time home buyers will primarily be felt in the more affordable, sectional title market – a sector of the market typically favoured by first-time buyers.

With consumer confidence recovering slightly, inflation and interest rates relatively subdued and the economy set to strengthen modestly in 2020, it seems likely that the recent period of price adjustment has seen a measure of affordability return to much of the national housing market – making it a good time to buy.

While the market is showing tentative signs of stabilising and with some recovery in house price inflation evident in the Western Cape in particular and in the Tshwane to a lesser extent, the market is unlikely to experience a robust recovery until there is a marked improvement in economic growth prospects and employment – because the housing market is not only driven by the willingness of residents to buy but also their ability – which requires growth and employment (as well as financial institutions willing to extend credit).

Market consensus forecasts are for slightly stronger economic growth in 2020 and beyond. While inflation may be somewhat higher than this year, it is not expected to force the Reserve Bank to raise interest rates during the next 12-18 months. Add to this the ongoing appetite among financial institutions to extend credit, and there are a number of factors underpinning the market next year.

Given that any recovery in the housing market is likely to be modest, now more than ever it is advisable for homeowners to focus on location and minimal overheads (security, maintenance and utilities). With household incomes under pressure and growing congestion, well-located growth nodes are increasingly appealing for convenience, reduced transport costs and future return on investment, when selling or renting out.

Coupled with this, as water and energy remain an issue (both in terms of availability and cost, homes with energy and water efficiency – green features), or located within a development or estate with green amenities are likely to become increasingly attractive to buyers and add value on future resale.

The outlook for 2020 is for a better housing market but only moderately better than 2019 – unless economic growth surprises on the upside, however, with professional advice and considered options, savvy investment and selling decisions are definitely achievable.

For further information contact Pam Golding Properties on 021 7101700 or email headoffice@pamgolding.co.za.

Posted by The Know - Pam Golding Properties

Housing assets reflect a further recovery in price appreciation

Thursday 5th of June 2025

Very welcome interest rate relief for consumers – including home buyers and mortgage applicants

Thursday 29th of May 2025

Majority of first-time buyers still purchase freehold homes

Friday 16th of May 2025